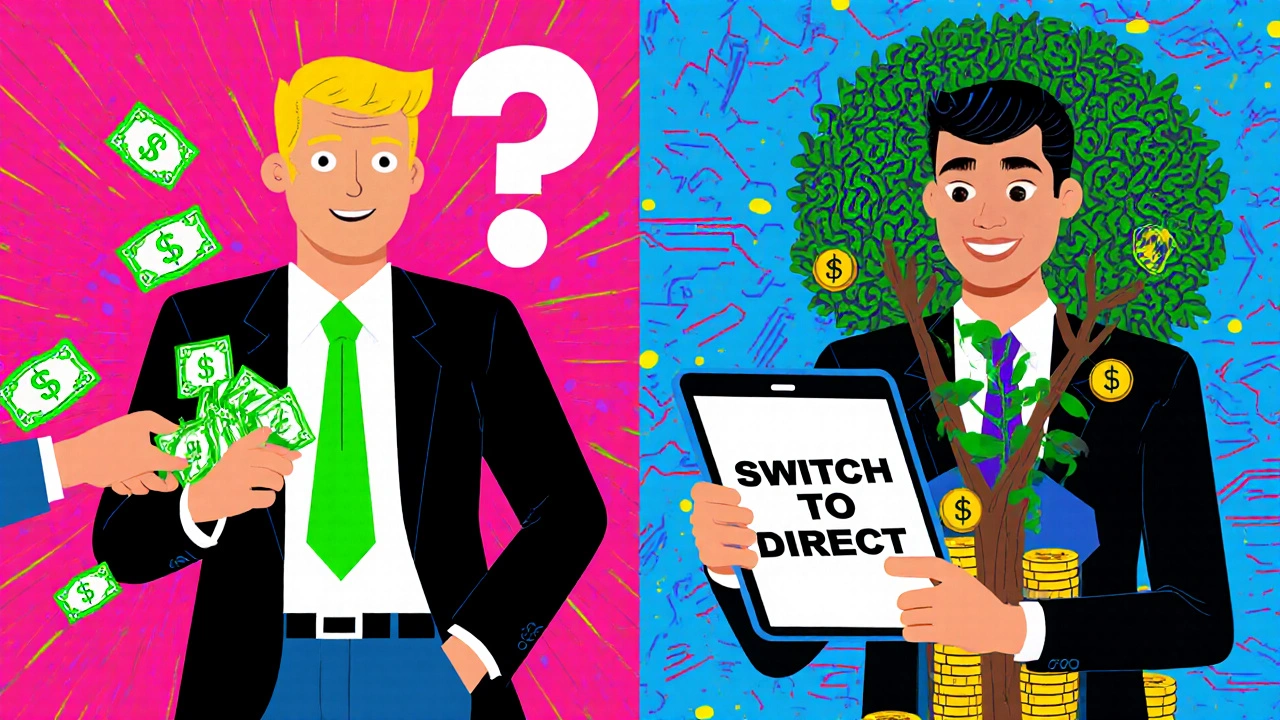

Direct Plan vs Regular Plan: What’s the Real Difference for Indian Investors?

When you invest in mutual funds in India, you’re choosing between two paths: a direct plan, a mutual fund investment route where you buy directly from the fund house without any intermediary, or a regular plan, a version sold through advisors, distributors, or platforms that charge a commission. The difference isn’t just paperwork—it’s your money. A direct plan cuts out the middleman, so your returns aren’t reduced by hidden fees. A regular plan includes those fees, often buried in the expense ratio, which can eat up 0.5% to 1.5% of your returns every single year. Over 10 years, that’s tens of thousands of rupees you could’ve kept.

Here’s how it works in practice: if you invest ₹5 lakh in a fund with a 1.2% expense ratio under a regular plan, you’re paying ₹6,000 a year just in fees. Switch to a direct plan with a 0.5% expense ratio, and that drops to ₹2,500. That’s ₹3,500 extra in your pocket annually, compounding over time. This isn’t theory—it’s math. And it’s why people who switch from regular to direct plans often see their portfolio grow faster, even if they don’t change their investment amount. The expense ratio, the annual fee charged by the fund house to manage your money is the key number to check. It’s listed in the fund factsheet, and it’s higher in regular plans because it includes distributor commissions. Some platforms still push regular plans because they earn more from them, not because they’re better for you.

Who should pick which? If you’re comfortable researching funds, tracking performance, and managing your portfolio yourself, a direct plan is the clear winner. You save money, and you keep full control. If you rely on an advisor for guidance—someone who helps you pick funds, rebalance, or stay calm during market swings—then a regular plan might make sense, as long as you know exactly what you’re paying for. But don’t assume the advisor is working in your best interest just because they’re offering advice. Many push funds that pay them higher commissions, not the ones with the best returns. Always ask: ‘Is this fund in the direct plan too?’ If they say no, or avoid answering, that’s a red flag.

You’ll find posts below that dig into exactly how these plans affect your returns, what fees you’re really paying, and how to switch from regular to direct without penalties. We’ve covered the real cost of advisor commissions, how to spot hidden charges, and why even small differences in expense ratios matter more than you think. Whether you’re new to mutual funds or have been investing for years, this isn’t about complexity—it’s about making sure your money works harder for you.

Direct vs Regular Mutual Funds in India: Save More with Direct Plans

Direct mutual funds in India save you thousands by cutting out advisor commissions. Learn how direct vs regular plans work, how much you can save, and how to switch today.

Categories

- Cryptocurrency

- Careers & Education

- Home & Living

- Technology

- Home & Lifestyle

- hire domestic help in Mumbai

- hire drivers in mumbai

- Personal Finance

- hire pet care in mumbai

- Travel & Transportation