How to Combine Section 80C and 80CCD in India to Maximize Your Tax Deductions

Jan, 13 2026

Jan, 13 2026

Every year, millions of salaried Indians miss out on thousands of rupees in tax savings-not because they don’t earn enough, but because they don’t know how to stack their deductions properly. The key? Combining Section 80C and Section 80CCD the right way. These two sections aren’t just separate rules-they’re designed to work together. When used in sync, they can unlock up to ₹2.5 lakh in annual tax deductions under the old tax regime. Even under the new regime, smart planning still gives you room to cut your taxable income significantly.

What Section 80C Actually Covers

Section 80C is the most popular tax-saving tool in India. It lets you deduct up to ₹1.5 lakh from your gross income for investments and expenses like:

- Public Provident Fund (PPF)

- Employee Provident Fund (EPF) contributions

- Life insurance premiums

- Equity Linked Savings Scheme (ELSS) mutual funds

- Fixed deposits (5-year tenure)

- Tuition fees for children

- Principal repayment on home loans

But here’s the catch: this ₹1.5 lakh limit is shared across all these options. If you put ₹1 lakh into PPF and ₹50,000 into ELSS, you’ve already used up your entire 80C limit. No more room for other deductions under this section.

Section 80CCD: The Hidden Bonus

Section 80CCD is where most people get confused. It’s not a replacement for 80C-it’s an add-on. There are two parts:

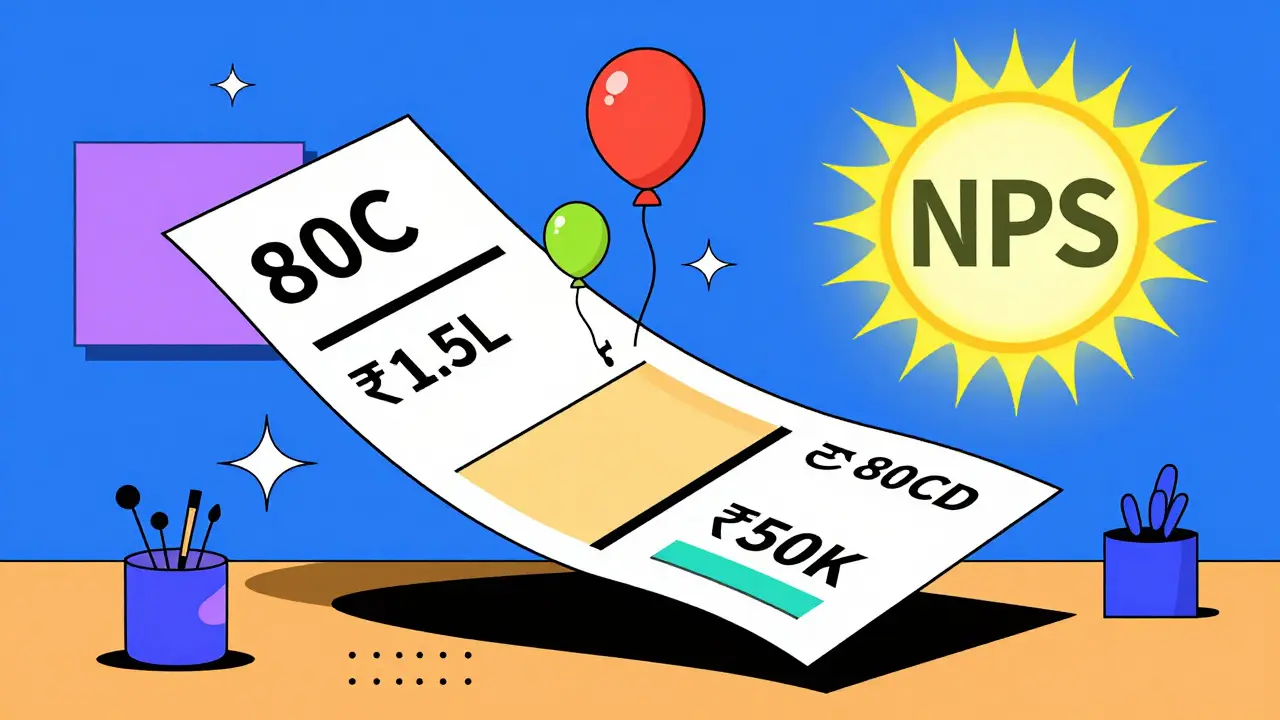

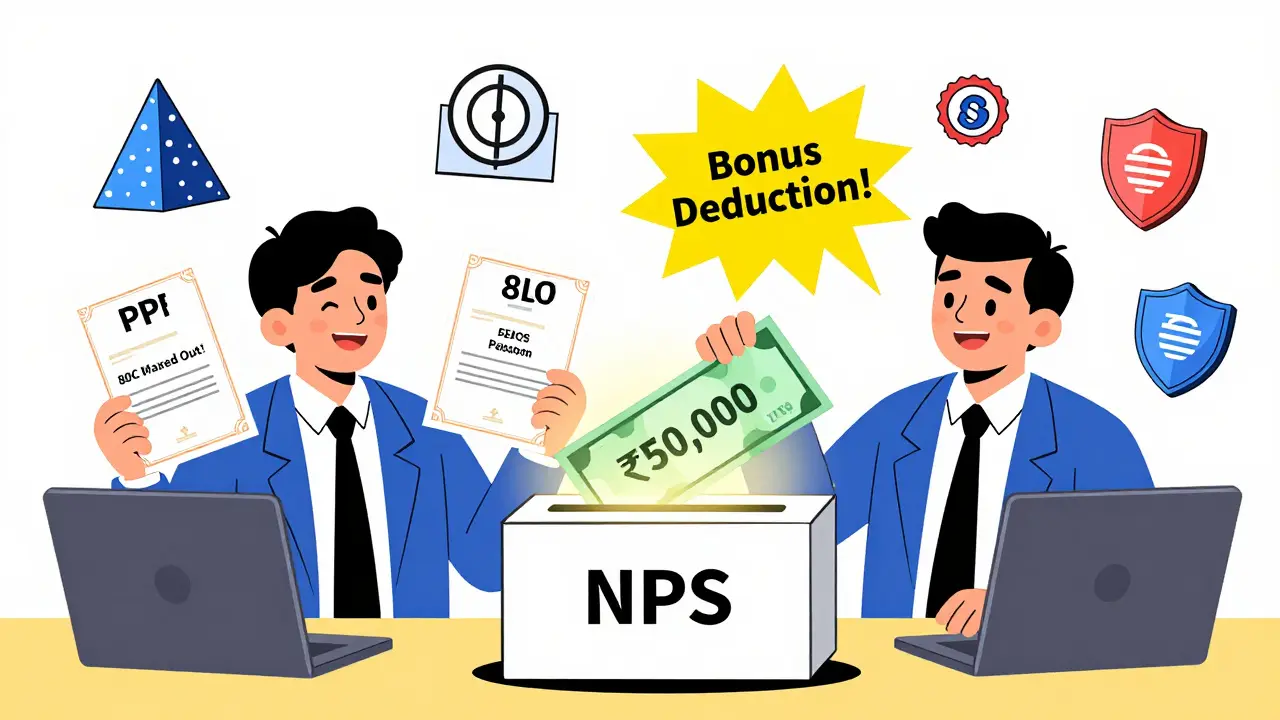

- 80CCD(1): Lets you claim up to ₹50,000 for contributions to the National Pension System (NPS), over and above your ₹1.5 lakh under 80C.

- 80CCD(2): Covers your employer’s contribution to your NPS account. This is separate and has no cap under the old regime.

So if you’re employed and your company contributes ₹10,000 annually to your NPS, that ₹10,000 doesn’t eat into your 80C or 80CCD(1) limit. It’s extra. And if you personally invest ₹50,000 into NPS, you get an additional ₹50,000 deduction on top of your ₹1.5 lakh under 80C.

Putting It Together: The Real Math

Let’s say you’re a salaried employee earning ₹12 lakh per year. Here’s how you can legally reduce your taxable income:

- Invest ₹1.5 lakh in 80C-eligible instruments: PPF, ELSS, insurance, etc.

- Contribute ₹50,000 to NPS under 80CCD(1).

- Your employer contributes ₹75,000 to your NPS under 80CCD(2).

Total deduction: ₹1.5 lakh + ₹50,000 + ₹75,000 = ₹2.75 lakh.

That’s not theoretical. This is how mid-to-high income earners in India actually reduce their tax liability. Under the old regime, this could mean saving up to ₹82,500 in taxes (at 30% slab), depending on your income and other deductions.

Even if you’re on the new tax regime (which has lower rates but no 80C deductions), you can still use 80CCD(1) and 80CCD(2) to claim up to ₹75,000 in deductions-₹50,000 from your own NPS contribution and ₹25,000 from your employer’s (if they match up to that). So even if you’ve switched to the new regime, NPS still gives you an edge.

What You Can’t Do

There are common myths that lead to mistakes:

- Myth: You can claim ₹1.5 lakh under 80C and another ₹1.5 lakh under 80CCD(1). Reality: 80CCD(1) is capped at ₹50,000 over and above 80C.

- Myth: Only government employees get employer NPS contributions. Reality: Many private companies now offer NPS as part of CTC, especially in IT, banking, and manufacturing.

- Myth: NPS is risky because it’s market-linked. Reality: NPS allows you to choose your asset allocation-up to 75% in equities if you’re under 50. You control the risk.

Also, don’t confuse 80CCD with 80CCC. That’s for pension annuity plans from insurance companies. It’s part of the ₹1.5 lakh 80C limit, not extra. Stick to NPS for the real bonus.

How to Set It Up

Here’s a simple step-by-step plan:

- Check your salary slip. Does it show an NPS contribution from your employer? If yes, note the amount.

- Calculate how much you’ve already used under 80C. Use your Form 16 or investment statements.

- Decide how much more you can invest in NPS. Aim for ₹50,000 to get the full 80CCD(1) benefit.

- Open an NPS account through a Point of Presence (PoP)-banks like SBI, HDFC, or online platforms like NSDL or CAMS.

- Link your NPS to your PAN and Aadhaar. Make sure contributions are made via your own bank account to qualify for deduction.

- Keep receipts and statements. You’ll need them when filing your ITR.

Pro tip: Invest in NPS early in the financial year. That way, you avoid last-minute rush, and your money gets more time to grow.

Why NPS Is Worth the Effort

NPS isn’t just a tax tool. It’s a retirement plan. Unlike PPF or FDs, NPS offers higher growth potential because of its equity exposure. Over 20-25 years, even ₹50,000 a year can grow into over ₹1.5 crore at 9-10% annual returns.

Plus, when you retire, you can withdraw 60% tax-free. The remaining 40% must go into an annuity, which gives you a monthly pension. The annuity income is taxable, but your monthly payout will likely fall in a lower tax bracket than your working years.

And unlike ELSS, which has a 3-year lock-in, NPS locks your money until 60-but you can withdraw 25% early after 10 years if you leave your job. That flexibility makes it better than most long-term savings tools.

Who Should Skip This?

Not everyone needs to chase the full ₹2.5 lakh deduction. If you’re earning under ₹7 lakh a year, the standard deduction and basic exemption might be enough. But if you’re in the 20% or 30% tax bracket, every rupee you deduct saves you 20 or 30 paise.

Also, if you’re already maxing out your 80C with high-risk investments like ELSS, adding NPS might feel like overkill. But think of NPS as your retirement safety net-low-cost, government-backed, and with tax benefits that don’t expire.

Common Mistakes to Avoid

- Investing in NPS through your employer’s portal without checking if it’s under Tier I (tax-eligible) or Tier II (no tax benefit).

- Forgetting to declare NPS contributions in your ITR under Schedule VI-A.

- Using the same money to claim both 80C and 80CCD(1)-you can’t double-dip. Each rupee counts once.

- Not tracking employer contributions. If your company adds ₹50,000 to your NPS, you’re already halfway to the 80CCD(2) benefit without spending a rupee.

Keep a simple spreadsheet: one column for 80C investments, one for your NPS contribution, one for employer’s contribution. Update it every quarter. That’s all it takes to stay on track.

What’s Changing in 2026?

As of 2026, there’s no official change to 80C or 80CCD limits. But the government is reviewing the entire tax structure to simplify compliance. Some proposals suggest merging 80C and 80CCD into a single ₹2 lakh limit, but nothing is confirmed yet.

Until then, the current rules stand. And if you’re planning to stay in India long-term, locking in the ₹2.5 lakh deduction now means you’re already ahead of any future changes.

Can I claim both 80C and 80CCD in the same financial year?

Yes. Section 80C gives you up to ₹1.5 lakh in deductions. Section 80CCD(1) adds another ₹50,000 specifically for your own contributions to NPS. These are separate limits. You can claim both in the same year.

Is NPS better than PPF for tax savings?

It depends. PPF gives you guaranteed returns (currently 7.1%) and is fully tax-free at maturity. NPS offers higher growth potential (historically 8-10%) but is market-linked. For tax savings, NPS gives you an extra ₹50,000 deduction under 80CCD(1), which PPF doesn’t. So if you’ve already maxed out 80C, NPS is the better next step.

Can self-employed people claim Section 80CCD?

Yes. Self-employed individuals can contribute up to ₹50,000 to NPS under 80CCD(1) and claim the deduction. However, they don’t get the employer contribution part (80CCD(2)) since they’re not employed by someone else.

What happens if I withdraw from NPS before 60?

You can withdraw up to 25% of your own contributions tax-free after 10 years if you leave employment. The rest must remain invested until 60. Early withdrawal of employer contributions or annuity funds is not allowed. Any premature withdrawal beyond the allowed 25% is taxable.

Do I need to file ITR to claim 80CCD deductions?

Yes. Even if your employer has deducted TDS based on your declarations, you must report your NPS contributions under Schedule VI-A in your ITR. Without this, the Income Tax Department won’t recognize the deduction.