How to Rebalance a Retirement Portfolio in India: Practical Annual Steps

Mar, 15 2026

Mar, 15 2026

Retirement isn’t something you plan for once and forget. In India, where life expectancy is rising and pension systems are still evolving, your retirement portfolio needs regular attention. If you’ve been investing in mutual funds, NPS, EPF, or fixed deposits, you might be surprised how much your asset mix has drifted from your original goal. That’s where rebalancing comes in. It’s not about timing the market. It’s about staying on track. And doing it once a year can make all the difference.

Why Rebalancing Matters in India

Imagine you started your retirement journey in 2020 with a 60/40 split: 60% in equity mutual funds, 40% in debt instruments like PPF or fixed deposits. Over the next few years, the stock market surged. By 2025, your equity portion grew to 78% of your portfolio. That’s not a win-it’s a risk. You’ve become way more exposed to market crashes than you planned for. Now, if the market drops 20%, you could lose years of gains overnight. Rebalancing fixes that. It brings your portfolio back to the risk level you’re comfortable with.

In India, where emotional investing is common-people panic-sell during downturns or chase hot stocks-rebalancing acts as a built-in discipline. It forces you to sell high and buy low, without letting fear or greed drive decisions.

Your Annual Rebalancing Checklist

Here’s what to do every year, around the same time-say, your birthday or the start of the financial year.

- Take stock of your current holdings-list every account: EPF, NPS, mutual funds, fixed deposits, gold ETFs, even real estate if it’s part of your retirement plan. Note the current value of each.

- Calculate your current allocation-add up the total value of your portfolio. Then divide each asset’s value by the total. For example, if your equity funds are worth ₹48 lakh and your total portfolio is ₹80 lakh, your equity exposure is 60%.

- Compare with your target-what was your original goal? 70% equity, 30% debt? Or 50/50? If you’re within 5 percentage points, you’re fine. If you’re outside that range, it’s time to adjust.

- Decide how to rebalance-do you sell some equity and move cash into debt? Or do you redirect new contributions? Selling might trigger capital gains tax. Redirecting new money is often simpler and tax-efficient.

- Execute the shift-use SIPs, lump-sum transfers, or redemption requests. For NPS, you can change your asset allocation via the NSDL portal. For mutual funds, use the fund house’s website or a platform like Zerodha or Groww.

What Should Your Target Allocation Be?

There’s no one-size-fits-all rule. But here’s a simple formula used by many financial planners in India:

100 minus your age = equity percentage

So if you’re 45, aim for 55% in equity and 45% in debt. If you’re 58, go for 42% equity and 58% debt. This is a starting point. Adjust based on your risk tolerance. If you sleep well during market crashes, you can go 10% higher in equity. If a 5% drop keeps you awake, dial it back.

Also consider your retirement timeline. If you’re 10 years away, you can afford more risk. If you’re 3 years out, start shifting toward safety. Liquid assets like fixed deposits, short-term debt funds, and NPS Tier-I (with government-backed security) become more important.

Where to Rebalance: NPS, Mutual Funds, EPF

Each investment tool has its own rebalancing rules.

- NPS (National Pension System): You can change your asset allocation once a year. Go to the NPS portal, log in, and adjust the percentage between equity (E), corporate bonds (C), and government securities (G). Most people stick with 50% E, 30% C, 20% G. But if you’re under 50, 60% E is common.

- Equity mutual funds: These are easy to rebalance. Sell units from overperforming funds and buy into underweight ones. Watch out for exit loads and LTCG tax (12.5% on gains above ₹1.25 lakh per year).

- EPF: You can’t rebalance EPF-it’s 100% debt, with a fixed interest rate (8.25% in 2025). But you can use it as your anchor. If your EPF balance is growing fast, you may need to reduce other debt holdings to stay balanced.

- Fixed deposits and gold: These are stable but low-return. If they’ve grown too large, consider using new contributions to buy more equity instead of adding to FDs.

Tax Implications You Can’t Ignore

Rebalancing isn’t free. In India, selling mutual fund units triggers taxes.

- Equity funds: If held over 1 year, gains above ₹1.25 lakh are taxed at 12.5%. This is LTCG. You can use this threshold wisely-sell just enough to rebalance without crossing it.

- Debt funds: If held under 3 years, gains are added to your income and taxed at your slab rate. If held over 3 years, they’re taxed at 20% with indexation. Rebalancing within debt funds is usually tax-neutral.

- Gold ETFs: Treated like debt funds. 3-year holding period for indexation benefits.

Pro tip: Use new contributions to rebalance instead of selling. For example, if your equity is 75% instead of 60%, put next year’s SIP money entirely into debt funds. It’s slower but tax-smart.

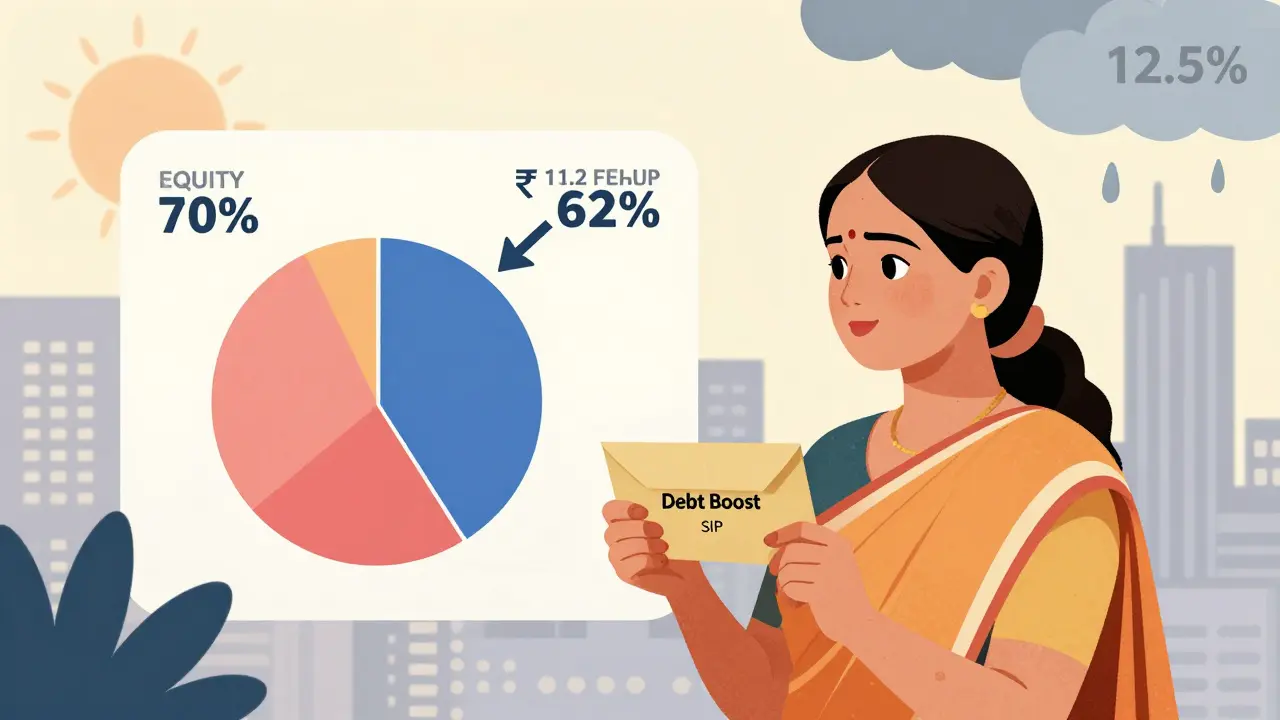

Real Example: Priya’s Story

Priya, 48, from Pune, started her retirement portfolio in 2018 with ₹30 lakh. Her target: 60% equity, 40% debt. By 2025, her equity had grown to ₹42 lakh, debt to ₹18 lakh. That’s 70% equity. Too risky. She didn’t want to sell and pay tax. So she redirected her ₹1.2 lakh annual SIP into debt funds. In two years, her equity dropped to 62%. No tax. No stress. Just steady correction.

Common Mistakes to Avoid

- Rebalancing too often-monthly or quarterly changes lead to unnecessary taxes and transaction fees.

- Ignoring inflation-your retirement goal isn’t ₹1 crore today. It’s ₹2.5 crore in 15 years. Rebalancing keeps you on that path.

- Chasing performance-if your small-cap fund doubled, don’t pour more into it. Stick to your plan.

- Forgetting insurance-your term plan and health insurance aren’t part of your portfolio. But they protect it. Make sure they’re up to date before you rebalance.

When to Skip Rebalancing

You don’t need to rebalance every year if:

- Your portfolio is under ₹5 lakh-transaction costs and taxes may eat into returns.

- You’re within 3% of your target-no need to move money for small drifts.

- You’re in a major market crash and your equity is down 30%-wait. This is a buying opportunity, not a rebalancing moment. Buy more, don’t sell.

Final Thought: It’s About Consistency, Not Timing

Rebalancing isn’t a magic trick. It doesn’t promise higher returns. It promises steadier returns. In India, where markets swing wildly and personal finance advice is often conflicting, sticking to a simple annual ritual gives you control. You’re not trying to beat the market. You’re just trying to stay in the game. And that’s how most people retire with dignity-not by luck, but by routine.

How often should I rebalance my retirement portfolio in India?

Once a year is ideal. More often increases taxes and fees. Less often lets your portfolio drift too far from your risk goals. Many Indians choose to rebalance around their birthday or at the start of the financial year (April 1). This creates a consistent habit.

Can I rebalance without paying taxes?

Yes. Instead of selling existing investments, redirect new contributions. For example, if your equity is too high, put your next SIP or bonus into debt funds. This slowly brings your allocation back in line without triggering capital gains tax. It takes longer, but it’s smarter in India’s tax environment.

Is NPS better than mutual funds for retirement?

NPS offers lower fees, tax benefits under Section 80CCD(1B), and government-backed security. But mutual funds give you more control over asset choice and timing. Most Indians use both: NPS for the core, stable portion, and mutual funds for growth. The best strategy combines both, not picks one.

What if I miss my annual rebalancing?

Don’t panic. Just do it the next year. A delay of 6-12 months won’t ruin your plan. The key is to get back on schedule. Set a calendar reminder. Rebalancing is a habit, not a deadline. Consistency over time matters more than perfect timing.

Should I include my home in my retirement portfolio?

Only if you plan to sell it in retirement to fund your lifestyle. If you’re living in it, don’t count it as an investment-it’s an expense. But if you own a second property you intend to rent or sell, include its value in your portfolio. Most Indians rely on EPF, NPS, and mutual funds for retirement income-not property.