National Savings Certificate (NSC) in India: Government-Backed 80C Investment Option

Dec, 17 2025

Dec, 17 2025

When you’re looking for a safe place to park your money in India - one that’s backed by the government, gives you tax breaks, and doesn’t require you to be a finance expert - the National Savings Certificate (NSC) stands out. It’s not flashy. It doesn’t promise quick returns. But for millions of middle-income families, it’s the quiet, reliable choice that helps them build savings while cutting their income tax bill under Section 80C of the Income Tax Act.

What Exactly Is an NSC?

The National Savings Certificate is a small savings scheme issued by the Government of India through post offices. It’s been around since 1957, and it hasn’t changed much because it doesn’t need to. It’s simple: you invest a lump sum, earn fixed interest over five years, and get your money back with interest at maturity. The government guarantees both your principal and the returns. That means no risk of default - not even during a market crash.

Unlike mutual funds or stocks, NSC doesn’t depend on market performance. There’s no fund manager to pay. No volatility. Just a fixed interest rate set by the Ministry of Finance every quarter. As of January 2025, the rate is 7.7% per annum, compounded annually. That’s higher than most bank fixed deposits and far safer than corporate bonds.

How Does NSC Help You Save Tax Under Section 80C?

Section 80C of the Income Tax Act lets you claim a deduction of up to ₹1.5 lakh per year on certain investments and expenses. NSC is one of the most popular options under this rule. When you buy an NSC, the amount you invest - up to ₹1.5 lakh - reduces your taxable income.

Let’s say you earn ₹12 lakh a year and invest ₹1 lakh in NSC. Your taxable income drops to ₹11 lakh. If you’re in the 20% tax bracket, that’s ₹20,000 saved in taxes right away. That’s not a small win.

Here’s the catch: the interest earned on NSC is taxable. But here’s the trick - you can claim the interest as a reinvestment each year under Section 80C. That means you’re not just getting tax-free growth - you’re also getting a fresh 80C deduction every year for the interest accrued. This is called the “interest reinvestment benefit.” It’s not automatic; you have to declare it in your tax return. But if you do, you’re effectively compounding your tax savings.

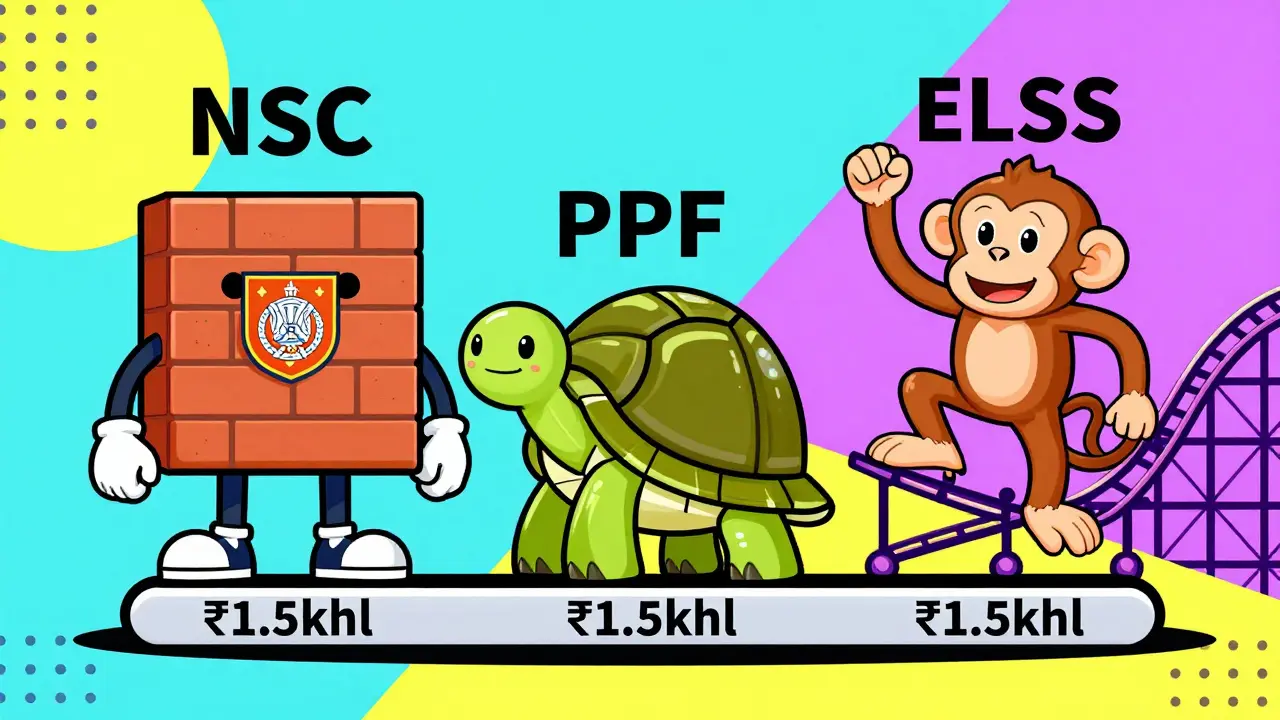

NSC vs Other 80C Options: What’s Better?

There are over a dozen options under Section 80C: PPF, ELSS, life insurance premiums, tuition fees, home loan principal, and more. So why choose NSC?

Here’s how it stacks up:

| Feature | NSC | PPF | ELSS Mutual Funds | Bank FD |

|---|---|---|---|---|

| Lock-in Period | 5 years | 15 years | 3 years | 5+ years (for 80C) |

| Interest Rate | 7.7% | 7.1% | Variable (avg 10-12%) | 6.5-7.5% |

| Government Backing | Yes | Yes | No | No |

| Tax on Interest | Taxable (but reinvestable) | Exempt | Taxable (if held >1 year) | Taxable |

| Liquidity | Low (only after 5 years) | Very Low | Medium | Low (penalty for early withdrawal) |

| Minimum Investment | ₹100 | ₹500 | ₹500 | ₹1,000 |

NSC wins on simplicity and safety. If you’re risk-averse and want guaranteed returns with a decent tax break, it’s hard to beat. PPF has a longer lock-in and lower rates. ELSS gives higher returns but comes with market risk - and you need to monitor it. Bank FDs are similar in rate, but you don’t get the same 80C advantage unless you pick a 5-year FD, and even then, the interest is fully taxable.

Who Should Invest in NSC?

NSC isn’t for everyone. It’s perfect for:

- People who want guaranteed returns without market exposure

- Salaried employees looking to reduce their taxable income

- Parents saving for their child’s education or marriage

- Retirees seeking a steady, low-risk income stream

- Anyone who doesn’t want to manage investments actively

If you’re young, aggressive, and already investing in mutual funds or stocks, NSC might not be your top priority. But if you’re building a foundation - or just want to lock in tax savings without thinking about it - NSC is a no-brainer.

How to Buy NSC in 2025

Buying an NSC is straightforward. You can do it at any post office in India. You’ll need:

- A valid ID (Aadhaar, PAN, passport)

- A completed Form 1 (available at the post office)

- The investment amount in cash, check, or digital payment

You can buy NSC in your name, or in the name of a minor (with you as guardian). Joint holdings aren’t allowed. The minimum investment is ₹100. There’s no upper limit per transaction, but the total 80C deduction is capped at ₹1.5 lakh per year. So if you invest ₹2 lakh, only ₹1.5 lakh will count for tax deduction.

After purchase, you’ll get a certificate - either physical or electronic. Most post offices now issue e-NSC via the India Post Payments Bank app. Keep this safe. You’ll need it to claim interest reinvestment and for maturity claims.

What Happens at Maturity?

After five years, the NSC matures. You can withdraw the full amount - principal plus interest - in one go. The interest is paid out automatically. If you don’t withdraw, the amount stays in the post office account at the savings account rate (currently 4% per annum), which is much lower.

You can also choose to reinvest the maturity amount into a new NSC. That’s a common strategy for retirees who want to keep their money working without touching the principal.

Can You Withdraw NSC Early?

Not easily. NSC has a strict 5-year lock-in. But there are two exceptions:

- If the holder dies, the nominee can claim the amount before maturity.

- If the holder is declared insolvent or is a government employee transferred abroad, you can apply for premature encashment - but only with approval from the postmaster.

Otherwise, early withdrawal isn’t allowed. That’s why it’s important to only invest money you won’t need for five years.

Common Mistakes People Make With NSC

Even though NSC is simple, people still mess it up:

- Not claiming interest reinvestment: Many don’t realize they can claim the yearly interest as a deduction. That’s leaving free tax savings on the table.

- Buying too late in the financial year: If you buy in March, you’ll miss out on the full year’s interest accrual. Buy in April or May for maximum benefit.

- Confusing NSC with Post Office Time Deposits: NSC is a certificate. Time deposits are FDs. Only NSC qualifies for 80C.

- Investing more than ₹1.5 lakh under 80C: Anything above ₹1.5 lakh doesn’t get tax benefit. Don’t waste money.

Is NSC Still Worth It in 2025?

With inflation at 5.2% and bank FDs offering 7% or less, NSC’s 7.7% rate looks strong. The government backing makes it safer than corporate bonds or even some PPF schemes. And the tax benefit? It’s real, reliable, and easy to claim.

It’s not going to make you rich. But if you’re serious about building wealth slowly and safely - and cutting your tax bill in the process - NSC remains one of the most underrated tools in India’s personal finance toolkit.

It’s not glamorous. But sometimes, the best investments aren’t the ones that make headlines. They’re the ones that quietly grow your money - year after year - without asking for attention.

Is NSC interest taxable?

Yes, the interest earned on NSC is taxable as income. However, you can claim the interest accrued each year as a reinvestment under Section 80C, which allows you to reduce your taxable income again. This effectively makes the interest tax-neutral over the five-year term if you reinvest annually.

Can I buy NSC online?

Yes, you can buy NSC online through the India Post Payments Bank (IPPB) app or website. You’ll need a registered account and a valid PAN. The process takes less than 10 minutes, and you’ll receive an e-certificate via email.

What happens if I lose my NSC certificate?

If you lose your physical certificate, you can apply for a duplicate at the post office where you bought it. You’ll need to submit a written request, proof of identity, and pay a small fee. For e-NSC, your certificate is stored digitally and can be re-downloaded anytime.

Can I invest in NSC for my child?

Yes, you can buy NSC in the name of a minor child. You’ll act as the guardian. The investment will count toward your own ₹1.5 lakh 80C limit. You cannot claim the deduction twice - once for yourself and once for your child.

Is NSC better than PPF?

NSC has a shorter lock-in (5 years vs. 15), slightly higher interest rate (7.7% vs. 7.1%), and easier access. But PPF offers tax-free interest and longer-term compounding. If you need liquidity sooner, NSC wins. If you’re saving for retirement, PPF is better. Many investors use both.