NPS Annuity Options in India: How to Choose the Right Pension at Retirement

Jun, 13 2026

Jun, 13 2026

You’ve spent decades contributing to your National Pension System (NPS), watching that corpus grow through market cycles. Now, you’re standing at the finish line of your career. The money is there, but how do you turn a lump sum into a steady paycheck that lasts as long as you do? This is where the choice gets critical. Getting it wrong could mean outliving your savings; getting it right means financial security for the rest of your life.

The government mandates that a significant portion of your NPS corpus must be used to buy an annuity. But "annuity" isn’t just one thing. It’s a menu of choices with different trade-offs regarding liquidity, inflation protection, and legacy planning. Let’s break down exactly what you can do with your money when you retire under the current regulations.

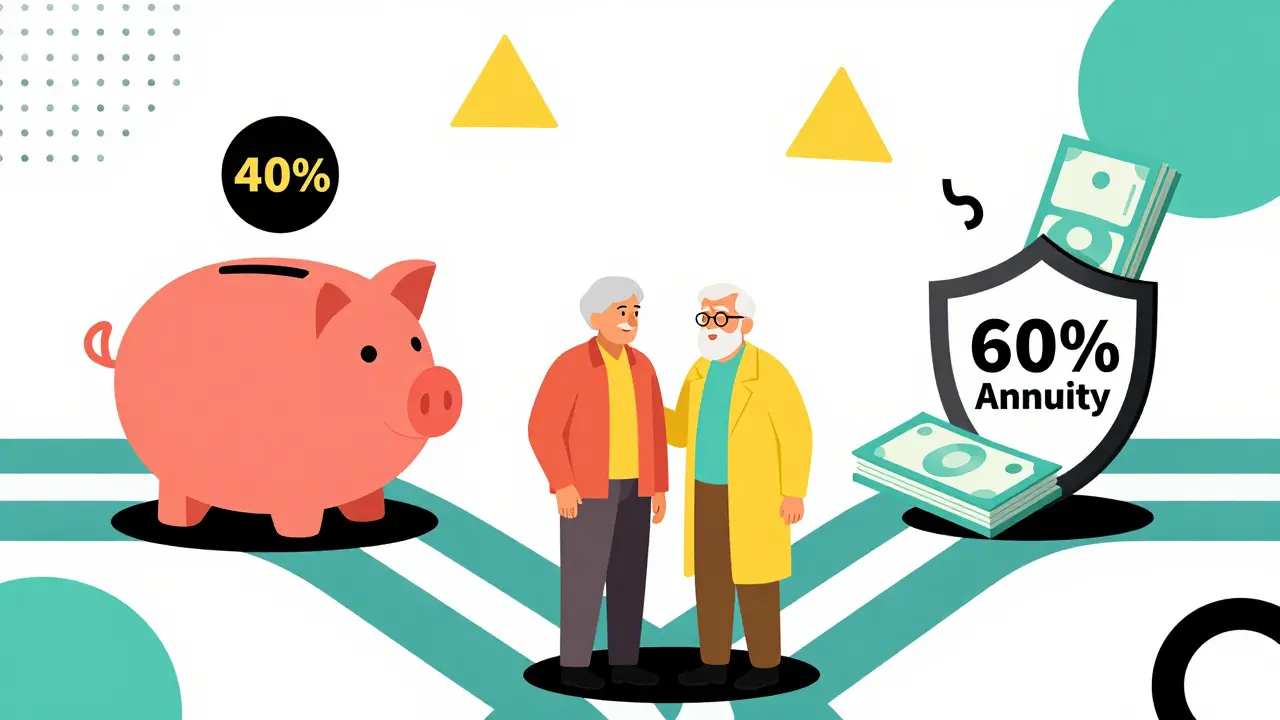

Understanding the Mandatory Annuity Rule

Before picking a plan, you need to understand the constraints. As of 2026, the rules for tax-resident subscribers are clear. When you withdraw from your NPS account upon reaching age 60, you cannot take everything as cash.

Here is the split:

- 40% Tax-Free Lump Sum: You can withdraw up to 40% of your total accumulated corpus as a tax-free lump sum. This is yours to keep, invest, or spend however you like.

- 60% Mandatory Annuity: The remaining 60% must be used to purchase an immediate annuity plan from an insurer approved by the Pension Fund Regulatory and Development Authority (PFRDA).

This rule exists to ensure you have a guaranteed income stream post-retirement. The goal is to prevent retirees from depleting their entire nest egg too quickly. If you are a non-resident Indian (NRI) or if you withdraw before age 60 due to specific reasons, the rules differ slightly, often requiring a larger percentage for annuitization. For this guide, we assume you are a standard resident retiree hitting the mark at 60.

What Is an Immediate Annuity?

An Immediate Annuity is a contract between you and an insurance company. You hand over a chunk of capital (your 60%), and in return, they promise to pay you a fixed monthly amount for a defined period or for the rest of your life. Think of it as buying your own salary.

The key feature here is certainty. Unlike mutual funds or stocks, which fluctuate daily, an annuity payout is stable. However, stability comes with a cost: you lose access to that principal capital. Once you buy the annuity, that money is locked in. You can’t sell the policy back to get the lump sum unless the specific plan allows it (which most don’t).

Types of Annuity Plans Available

Not all annuities are created equal. Insurers offer several variants based on your risk appetite and family situation. Here are the four main types you will encounter:

- Life Annuity Without Guarantee: This pays you monthly until you pass away. If you die next month, the payments stop, and the money goes to the insurer. If you live to 100, they keep paying. This usually offers the highest monthly payout because the insurer takes on the longevity risk.

- Life Annuity With Guaranteed Period (5, 10, or 15 years): This is the most popular choice. You receive payments for life. However, if you die within the first 5, 10, or 15 years (depending on what you choose), your nominee receives the remaining payments for that guaranteed period. After the guarantee expires, if you are still alive, payments continue. If you die after the guarantee, payments stop. This balances higher payouts with some protection for your family.

- Joint Life Annuity: Designed for couples. Payments continue for the lifetime of both spouses. Usually, there is a reduction factor (e.g., 20-30%) applied to the monthly payout compared to a single-life plan. Upon the death of the primary holder, the spouse continues to receive either the full amount or a reduced percentage (often 50% or 100%).

- Return of Purchase Price: In this variant, if you die before receiving the equivalent of your initial investment, the difference is paid to your nominee. This protects your capital but results in significantly lower monthly payouts.

Key Factors to Consider Before Buying

Choosing the right option isn’t just about picking the highest number on the sheet. You need to align the product with your personal reality. Ask yourself these questions:

| Factor | Why It Matters | Question to Ask Yourself |

|---|---|---|

| Inflation Protection | Fixed payouts lose purchasing power over time. | Do I have other assets (real estate, stocks) that will grow with inflation? |

| Health & Longevity | Longer life means more payouts from the insurer. | Is my family history indicative of long life? Do I have chronic health issues? |

| Spousal Dependence | Your partner may rely on this income after you’re gone. | Does my spouse have independent income or sufficient savings? |

| Liquidity Needs | Annuity capital is illiquid. | Is the 40% lump sum enough for emergencies and large expenses? |

Comparing Payout Rates: A Realistic Example

Let’s look at numbers. Suppose your total NPS corpus at age 60 is ₹50 Lakhs.

- Tax-Free Lump Sum (40%): ₹20 Lakhs

- Annuity Corpus (60%): ₹30 Lakhs

Assuming average annuity rates for a 60-year-old male in 2026 (rates vary by insurer and gender), here is what your monthly income might look like:

- Single Life Annuity (No Guarantee): Approx. ₹18,000 - ₹20,000 per month. (Highest payout, no legacy benefit)

- Single Life Annuity (10-Year Guarantee): Approx. ₹16,500 - ₹18,000 per month. (Balanced approach)

- Joint Life Annuity (100% to Spouse): Approx. ₹12,000 - ₹14,000 per month. (Lower payout, but secures spouse’s future)

Note that women typically receive slightly lower monthly payouts than men for the same corpus because actuarial tables show women live longer, meaning the insurer pays out for more years.

Who Should Avoid High-Guarantee Plans?

If you already have substantial other assets-like rental property, a separate portfolio of dividend-paying stocks, or a child who is financially established-you might not need the safety net of a long guarantee period. In this case, opting for a Life Annuity Without Guarantee or a short guarantee period (5 years) maximizes your monthly cash flow. You can use the extra monthly income to boost your lifestyle or invest further.

Conversely, if you have no other income sources and depend entirely on NPS, skipping the guarantee is risky. If you pass away early, your family loses that income stream completely. A 10 or 15-year guarantee ensures your family has breathing room to adjust finances even if something happens unexpectedly.

Common Mistakes to Avoid

1. Ignoring Inflation: A ₹15,000 payout today might feel comfortable, but in 20 years, it won’t cover basic groceries. Treat the annuity as your "floor" income. Use the 40% lump sum wisely to create an inflation-beating asset (like equity mutual funds) that supplements this fixed income.

2. Choosing the Wrong Insurer: While PFRDA regulates all approved insurers, their payout rates differ. Always compare quotes from at least three major players like LIC, SBI Life, ICICI Prudential, or HDFC Life. Even a 0.5% difference in rate can add up to thousands over a decade.

3. Overlooking Health Declarations: Some insurers ask for medical details for large annuity purchases. Be honest. Hiding pre-existing conditions can lead to claim disputes later. Most standard NPS annuities don’t require heavy medicals for amounts under ₹50 Lakhs, but check the specific policy terms.

Step-by-Step Guide to Purchasing Your Annuity

- Check Your Corpus: Log in to your Central Recordkeeping Agency (CRA) portal (NSDL or KFintech) to see your exact accumulated value.

- Decide on the Split: Confirm you are taking the maximum 40% tax-free withdrawal.

- Get Quotes: Contact 3-4 insurers. Provide your age, gender, and preferred annuity type. Ask for the "monthly pension amount" for a ₹30 Lakh corpus (or your actual 60% amount).

- Select the Plan: Choose based on the balance between monthly income and family security.

- Submit Application: Complete the KYC and application forms. Ensure your bank details for the pension credit are correct.

- Transfer Funds: The CRA will facilitate the transfer of the 60% amount directly to the insurer. You don’t handle the cash.

- Start Receiving Payments: The insurer will begin crediting your pension monthly, usually starting the month after the transaction is complete.

What About the 40% Lump Sum?

Don’t let the 40% sit idle in a savings account earning 3%. Since your annuity provides a fixed floor, this lump sum should work harder. Consider splitting it:

- Emergency Fund (10-15%): Keep 6-12 months of expenses in a liquid fund or high-yield savings account.

- Inflation Hedge (50-60%): Invest in a diversified mix of equity mutual funds or index funds. These historically outpace inflation over the long term.

- Debt/Stability (25-35%): Park this in arbitrage funds or corporate bond funds for moderate returns with lower volatility.

This hybrid approach gives you the peace of mind of a guaranteed pension plus the growth potential of active investments.

Can I change my annuity plan after buying it?

Generally, no. An immediate annuity is a long-term contract. Once purchased, you cannot switch to another insurer or change the type (e.g., from single to joint) without surrendering the policy, which often results in significant penalties or loss of value. Make sure you choose correctly the first time.

Is the annuity income taxable?

Yes. Unlike the 40% lump sum which is tax-free, the monthly pension received from the annuity is treated as "Income from Other Sources" and is added to your total annual income. It is taxed according to your applicable income tax slab rate.

What happens if I die shortly after buying the annuity?

It depends on the plan. If you chose a "Life Annuity Without Guarantee," the payments stop immediately. If you chose a plan with a guarantee period (e.g., 10 years), your nominee will receive the monthly payments for the remainder of that 10-year period. If you chose a Joint Life plan, your spouse continues to receive payments for their lifetime.

Can I buy an annuity from any insurance company?

You can only buy from insurers approved by the PFRDA. Major players include LIC, SBI Life, ICICI Prudential Life, HDFC Life, Max Life, and others. The list is publicly available on the PFRDA website. Stick to reputable companies with strong claim settlement ratios.

Do annuity rates increase over time?

Standard immediate annuities offer a fixed payout that does not increase. There are "escalating annuities" that offer a small annual increase (e.g., 3-5%), but these start with a much lower initial payout. Given high inflation in India, fixed annuities lose value over time, which is why supplementing with other investments is crucial.