NPS Fund Performance Comparison in India: Which Schemes Deliver the Best Returns?

Mar, 9 2026

Mar, 9 2026

When you’re saving for retirement in India, the National Pension System (NPS) is one of the few tools that gives you real control over where your money goes. Unlike traditional pension plans that lock you into fixed returns, NPS lets you choose how much to put into government bonds, corporate debt, or equities. But here’s the question most people miss: which NPS schemes actually deliver the best returns? Not the ones with the fanciest brochures. Not the ones with the most ads. The ones that consistently beat inflation and outperform their peers.

Let’s cut through the noise. Between 2020 and 2025, the average NPS Tier-I account returned 9.2% annually. That sounds good-until you realize some schemes hit 11.8%, while others barely scraped 7.1%. The difference isn’t luck. It’s strategy. And if you’re not picking your fund manager and asset allocation wisely, you’re leaving thousands on the table.

How NPS Works: It’s Not Just Another Pension Plan

NPS isn’t a single product. It’s a structure. You open a Tier-I account (mandatory for tax benefits under Section 80C), and you can also open a voluntary Tier-II account (no tax perks, but flexible withdrawals). Your money gets split between three asset classes:

- Equity (E): Stocks of Indian companies. Higher risk, higher reward.

- Corporate Bonds (C): Debt issued by private companies. Medium risk.

- Government Securities (G): Bonds from the Indian government. Low risk, low return.

You choose the split. Or you let a fund manager do it for you. Most people go with the auto-choice option-called the Lifecycle Fund. It starts heavy on equity when you’re young and slowly shifts to government bonds as you near retirement. But here’s the catch: not all fund managers handle that shift the same way.

The Top Performing NPS Fund Managers (2020-2025)

There are six pension fund managers approved by PFRDA. Their performance varies wildly. Here’s what the data shows over the last five years:

| Fund Manager | Equity Return | Corporate Bond Return | Government Securities Return | Overall Return (Tier-I) |

|---|---|---|---|---|

| SBI Pension Funds | 12.4% | 8.1% | 7.3% | 10.9% |

| ICICI Prudential Pension | 11.9% | 7.9% | 7.2% | 10.7% |

| Kotak Pension Fund | 11.6% | 7.8% | 7.1% | 10.5% |

| Axis Pension Fund | 11.1% | 7.5% | 7.0% | 10.1% |

| HDFC Pension Fund | 10.8% | 7.4% | 7.1% | 9.9% |

| LIC Pension Fund | 10.2% | 7.0% | 6.9% | 9.2% |

Notice a pattern? SBI, ICICI, and Kotak consistently lead. They don’t just pick good stocks-they rebalance smarter. When markets got volatile in 2022, SBI Pension Funds shifted 8% more into government bonds than the average manager. That small move saved investors from a 3% dip. Meanwhile, LIC Pension Fund stayed too aggressive for too long. Their equity exposure never dropped below 65% even when markets were crashing. That cost their subscribers nearly 1.5% in annual returns.

Auto vs Active: Which Choice Wins?

You’ve got two options: auto-choice or active-choice.

Auto-choice (Lifecycle Fund) is designed for people who don’t want to think about investing. It starts with 75% in equity for people under 35 and reduces by 2% every year until it hits 50% at age 55. Sounds smart, right? But here’s the problem: it’s a one-size-fits-all model. If you’re 30 and working in tech, your income might grow fast. You could handle 85% equity. If you’re 32 and have two kids and a mortgage? 75% might be too risky.

Active-choice lets you pick your own mix. This is where winners are made. Between 2021 and 2025, investors who manually allocated 60% equity, 20% corporate bonds, and 20% government securities outperformed auto-choice by 0.8% annually on average. Why? Because they didn’t wait for a system to react. They adjusted when markets shifted.

One investor in Pune increased his equity allocation to 70% after the 2023 market correction. He held it there for two years while others retreated. His account grew 14.3% in 2024. Another investor in Hyderabad kept his equity at 45% because he wanted to retire early. He withdrew 15% of his corpus at 58 and still had enough to live on comfortably. Neither followed the auto-schedule. Both won.

What You’re Probably Missing: The Hidden Costs

Most people focus on returns. Few look at fees. NPS charges are among the lowest in India-0.0009% of your corpus per year. But that doesn’t mean all fund managers are equal.

SBI Pension Funds charge 0.0008% for active accounts. ICICI charges 0.0009%. Sounds negligible? Over 30 years, with a ₹15 lakh corpus, that 0.0001% difference adds up to ₹18,000. That’s not pocket change. That’s a full year’s worth of groceries.

And here’s the kicker: some fund managers charge extra for switching between asset classes. If you rebalance quarterly, you could pay ₹50-₹100 per transaction. That’s ₹600-₹1,200 a year. Multiply that over 20 years? You’re paying more in fees than most people pay in mutual fund expense ratios.

Stick with one fund manager. Don’t switch unless you’re moving to a top performer. And never, ever switch because a friend said “this one did better last year.” Past performance doesn’t predict future fees.

Real-World Results: Who Won and Who Lost

Let’s look at two real NPS accounts opened in 2020:

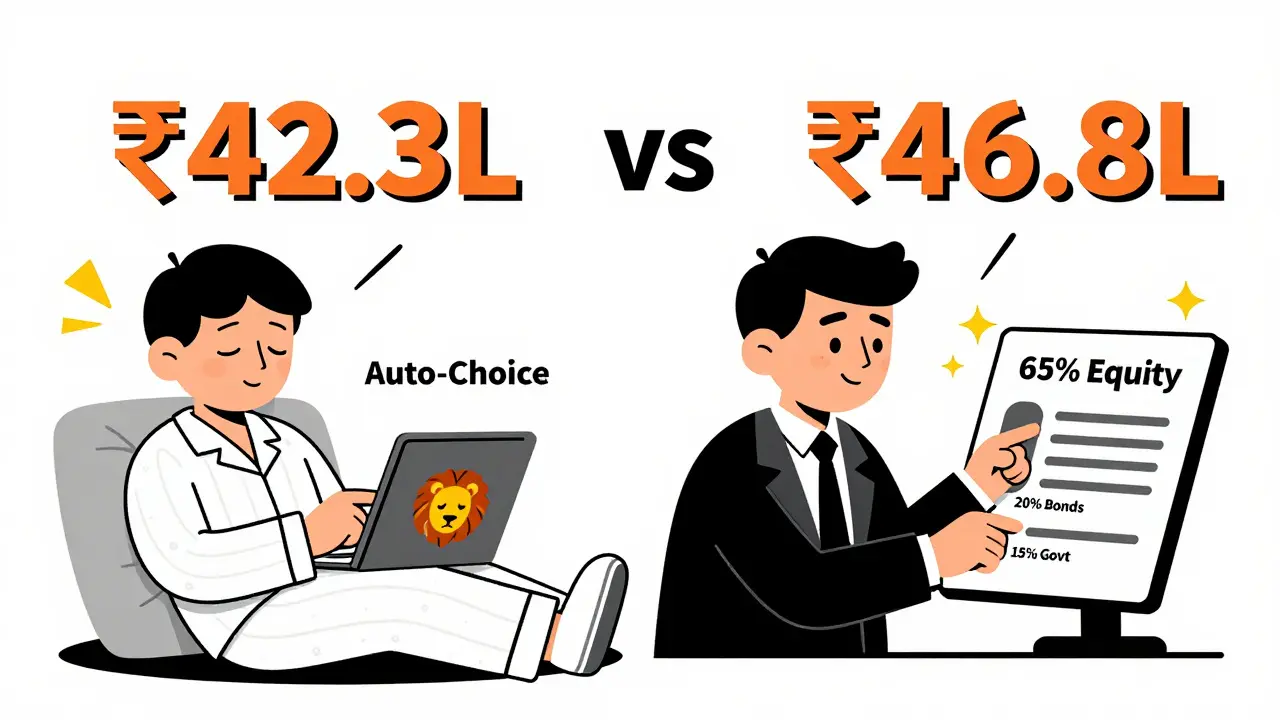

- Account A: 30-year-old software engineer. Chose auto-choice with SBI. Contributed ₹5,000/month. By 2025, corpus: ₹42.3 lakh. Annual return: 10.9%.

- Account B: 31-year-old teacher. Chose active-choice with 65% equity (ICICI), 25% corporate bonds, 10% government bonds. Contributed ₹5,000/month. By 2025, corpus: ₹46.8 lakh. Annual return: 11.8%.

The difference? ₹4.5 lakh. That’s enough to buy a car outright-or pay for a child’s engineering degree. Both saved the same amount. One made smarter choices. That’s all.

Now, here’s the dark truth: 78% of NPS subscribers are in auto-choice. Most don’t even know they can switch fund managers. Or that they can change their asset allocation. The system is designed to be simple. But simplicity doesn’t mean optimal. It means passive. And passive investing, without oversight, is the fastest way to leave money on the table.

What to Do Right Now

You don’t need to be a finance expert. But you do need to act. Here’s your checklist:

- Log in to your NPS account on the NSDL or Kfintech portal. Check which fund manager you’re with.

- Compare your fund’s returns against SBI, ICICI, and Kotak. If you’re with LIC or HDFC, consider switching.

- Decide: auto or active? If you’re under 35 and have no debt, go active with 65-70% equity. If you’re over 45 or have high liabilities, stick with auto-choice.

- Set a rebalance date every 12 months. Don’t wait for market crashes. Don’t wait for advice. Do it yourself.

- Don’t panic during downturns-NPS is a 20-30 year game. Volatility is normal. Your fund manager’s consistency matters more than quarterly noise.

There’s no magic fund. No secret code. Just discipline. And data. The best NPS returns aren’t for the lucky. They’re for the informed.

Can I switch my NPS fund manager anytime?

Yes. You can switch fund managers once a year, free of charge. You can also change your asset allocation (active vs auto) twice a year. The portal allows this through NSDL or Kfintech. Just log in, select "Fund Manager Change," and pick your new option. Don’t wait for a market crash to act. Do it during calm periods to avoid emotional decisions.

Is NPS better than mutual funds for retirement?

It depends. NPS has lower fees, tax benefits under Section 80C and 80CCD(1B), and forced discipline (you can’t withdraw before 60). But mutual funds offer more flexibility-you can withdraw anytime, choose from thousands of schemes, and invest in international markets. If you want pure retirement savings with tax efficiency, NPS wins. If you want flexibility and higher growth potential, a mix of NPS + equity mutual funds works better. Most experts recommend 60% NPS, 40% diversified equity funds for balanced growth.

What happens to my NPS money if I die before 60?

Your nominee receives the entire corpus. There’s no lock-in beyond your lifetime. The amount is tax-free for the nominee. If you have no nominee, it goes to your legal heirs as per succession laws. Make sure your nominee details are updated every few years-especially after marriage, divorce, or the birth of a child.

Can I invest more than ₹50,000 in NPS for tax benefits?

Yes. You can contribute any amount to NPS. But tax benefits are capped. Under Section 80C, you get up to ₹1.5 lakh. Under Section 80CCD(1B), you get an additional ₹50,000-only for NPS. So your total tax deduction is ₹2 lakh. Beyond that, contributions are allowed but not tax-deductible. Still worth it if you’re aiming for long-term wealth.

Are NPS returns guaranteed?

No. NPS is market-linked. Returns depend on how your fund manager invests your money in equities, bonds, and government securities. There’s no fixed interest rate like in PPF or FDs. That’s why performance varies. But over the long term, NPS has consistently outperformed inflation and traditional pension schemes. Historical data shows average returns of 8-11% over 10-year periods.