PPF Interest Credit and Tax Exemption in India: EEE Benefits Explained

May, 8 2026

May, 8 2026

You put money into a Public Provident Fund is a government-backed savings scheme in India that offers tax-free returns on long-term investments. You probably did it because you want to save for retirement or build a safety net without giving the Income Tax Department a cut of your profits. But there is a specific part of this deal that often gets overlooked: how exactly does the interest get credited, and why is the "EEE" tag so powerful? Understanding these mechanics isn't just about saving money; it’s about optimizing your wealth growth over fifteen years.

The magic of the PPF lies in its simplicity and its triple-layered tax shield. Unlike other investment vehicles where you pay tax on dividends or capital gains, the PPF ensures that every rupee you earn stays yours. This article breaks down the nitty-gritty of interest crediting, the EEE benefit structure, and what changes you need to watch out for as we move through 2026.

Understanding the EEE Tax Status

When financial advisors talk about the EEE tax status is a classification meaning Exempt-Exempt-Exempt, covering contributions, earnings, and withdrawals from an investment, they are referring to a unique advantage that very few instruments offer in India. Let’s break down what each "E" actually means for your wallet.

- First E (Contributions): Under Section 80C of the Income Tax Act is the primary legislation governing direct taxation in India, you can deduct up to ₹1.5 lakh per year from your taxable income. If you invest ₹1.5 lakh in PPF, you don’t pay tax on that amount. For someone in the 30% tax bracket, that’s an immediate ₹45,000 saving.

- Second E (Earnings): The interest you earn on your PPF balance is completely tax-free. There is no TDS (Tax Deducted at Source) on the interest, and you don’t have to declare it in your return. This is crucial because compound interest works best when nothing eats into the principal growth.

- Third E (Withdrawals): When you finally close the account after fifteen years, or take partial withdrawals later, the entire amount-principal plus accumulated interest-is tax-free. No capital gains tax, no exit load.

This triad makes PPF superior to many fixed-income alternatives like Fixed Deposits (FDs), where the interest is fully taxable according to your slab rate. In an FD, if you earn 7% but fall into the 30% tax bracket, your real return drops to roughly 4.9%. In PPF, you keep the full 7% (or whatever the current rate is).

How PPF Interest Is Credited Annually

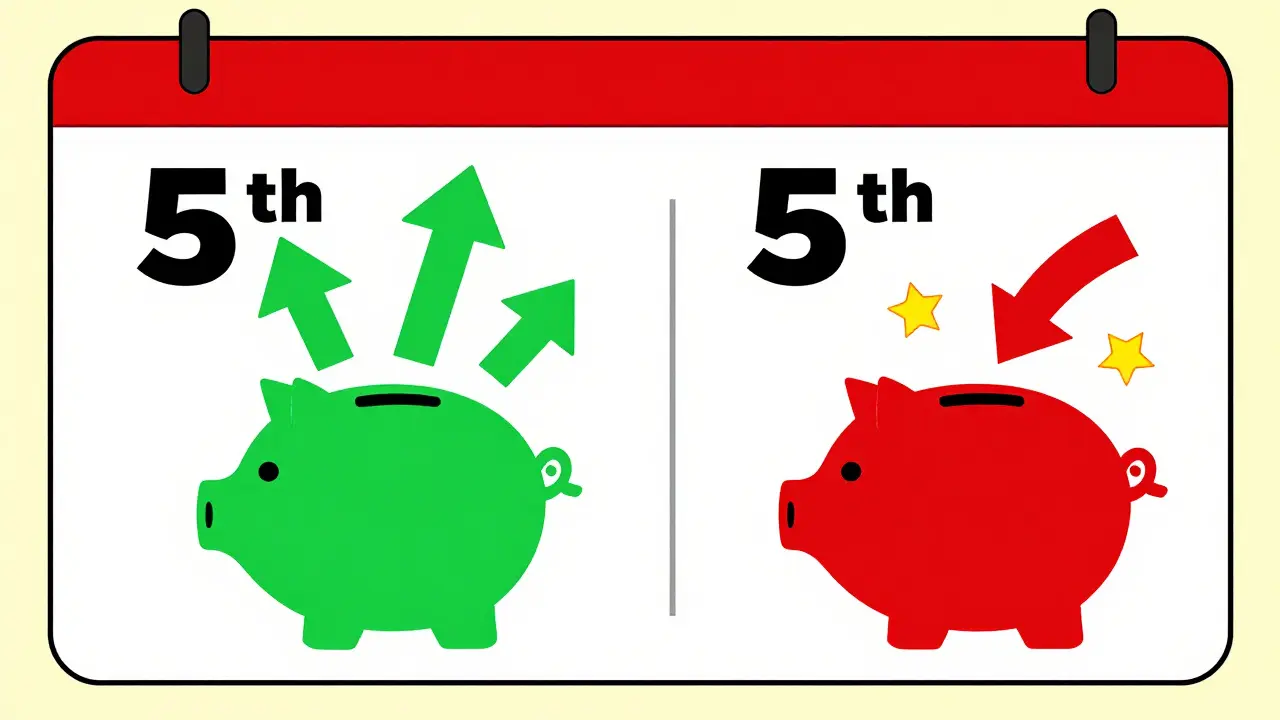

A common misconception is that the bank calculates your interest based on the highest balance held during the month. That’s not true. The interest crediting mechanism is the process by which the government calculates and adds interest to PPF accounts based on monthly balances relies on the lowest balance between the 5th day of the month and the end of the month.

Here is why that detail matters. If you deposit money on the 1st, 2nd, 3rd, or 4th of any month, it counts for that month’s interest calculation. If you deposit it on the 6th, 7th, or even the 30th, it won’t count until the next month. So, timing your deposits can literally add hundreds of rupees to your annual interest.

The interest rate is reviewed quarterly by the National Housing Bank is the apex regulatory body for housing finance institutions in India, which also sets PPF rates on behalf of the Government of India. As of early 2026, the rate has remained stable at 7.1% per annum. This rate is compounded annually and credited to your account at the end of the financial year, i.e., March 31st.

To maximize this, try to make your monthly or lump-sum contributions before the 5th of each month. Even if you only invest once a year, doing it on April 1st ensures you get interest for all twelve months. Doing it on April 6th means you lose one month’s interest. Over fifteen years, those lost months add up significantly due to the power of compounding.

Lock-in Period and Withdrawal Rules

The PPF is not a liquid asset. It comes with a strict lock-in period is a mandatory duration during which funds cannot be withdrawn from an investment account of fifteen years. However, the rules aren’t entirely rigid. You do have some flexibility, though it comes with conditions.

Starting from the seventh financial year after opening the account, you can make partial withdrawals. You can withdraw up to 25% of the balance at the end of the sixth preceding year, or 60% of the balance at the end of the third preceding year, whichever is lower. This is useful for emergencies like medical issues, education for children, or home repairs. But remember, the withdrawn amount stops earning interest, breaking the compounding chain.

If you absolutely need the money before fifteen years, you can close the account prematurely only under specific circumstances: permanent residency abroad, critical illness, or lack of employment due to ill health. In these cases, you must provide proof, such as a medical certificate or a letter from your employer confirming termination. The premature closure forfeits the tax exemption on the interest earned up to that point, meaning you’ll have to pay tax on the accumulated interest.

Extending Your PPF Account

What happens when the fifteen years are up? Many people think the account closes automatically. It doesn’t. At the end of the initial term, you can choose to extend the account for another five-year block. You can do this indefinitely.

You have two options when extending:

- Continue Contributing: You keep adding money (up to ₹1.5 lakh per year) and enjoy the same tax benefits and interest accrual.

- Stop Contributing: You stop putting in new money, but the existing balance continues to earn interest tax-free. This is a great strategy if you’ve already maximized your 80C limit elsewhere but still want a safe, growing corpus.

During the extension period, you can also make partial withdrawals. You’re allowed up to three withdrawals per year, subject to the same limits as the original term. This turns the PPF into a flexible retirement income source rather than just a lump-sum payout vehicle.

PPF vs. Other Retirement Instruments

Is PPF the best place for your retirement money? It depends on your risk appetite and liquidity needs. Here is how it stacks up against other popular choices in 2026.

| Feature | Public Provident Fund (PPF) | National Pension System (NPS) | Fixed Deposit (FD) |

|---|---|---|---|

| Tax Benefit on Contribution | Yes (₹1.5L under 80C) | Yes (₹1.5L under 80C + ₹50K under 80CCD(1B)) | No |

| Tax on Interest/Earnings | Exempt (EEE) | Deferred (Taxable on withdrawal) | Fully Taxable |

| Tax on Withdrawal | Exempt | 60% Tax-Free, 40% Taxable (unless annuity) | Fully Taxable |

| Liquidity | Low (15-year lock-in) | Very Low (Until age 60) | High (Anytime) |

| Risk Profile | Zero (Government Backed) | Medium to High (Market Linked) | Low (Bank Risk) |

| Current Returns (Approx.) | 7.1% p.a. | 8-10% p.a. (Variable) | 6.5-7.5% p.a. |

The NPS offers higher potential returns and an extra deduction of ₹50,000, but the withdrawal tax rules are complex. The FD gives you liquidity but destroys value through inflation and taxation. PPF sits in the middle: guaranteed, tax-free growth, but with low liquidity. For pure retirement planning, where you won’t touch the money for decades, PPF is hard to beat.

Who Should Open a PPF Account?

Not everyone needs a PPF account. If you are already maxing out your 80C limit with Life Insurance premiums or ELSS mutual funds, adding PPF might not give you additional tax benefits unless you shift allocations. However, if you are looking for a safe harbor for your emergency fund or a dedicated child’s education fund, PPF is ideal.

It is particularly beneficial for salaried employees who file under the old tax regime. With the new tax regime becoming more popular due to lower slab rates, the value of the 80C deduction has diminished for some. But the tax-free nature of the interest remains a massive advantage. Even if you don’t claim the deduction, the compounding effect of tax-free interest over 15-20 years creates a significant corpus compared to taxable instruments.

Also, consider the demographic. Young professionals starting their careers should open a PPF account early. Time is the biggest multiplier in compound interest. A ₹1 lakh investment made at age 25 grows to over ₹3.5 lakhs by age 60 at 7.1% interest. The same investment started at age 40 would only grow to around ₹1.3 lakhs. The earlier you start, the less you have to contribute to achieve the same goal.

Common Mistakes to Avoid

Even simple schemes have pitfalls. Here are the most common errors investors make with PPF:

- Missing the Minimum Contribution: You must deposit at least ₹500 per year. If you miss this, your account becomes inactive. To revive it, you have to pay a penalty of ₹50 for every year of inactivity, plus the minimum contribution for those years. Don’t let your account lapse.

- Ignoring Nominee Updates: PPF allows you to nominate a beneficiary. If you don’t update this after marriage, divorce, or the death of a nominee, the money can get tied up in legal probate. Update your nomination details whenever life events change.

- Overlooking Digital Access: Most banks now offer mobile apps for PPF management. Use them to track balances, make payments, and download statements. Paper trails are easy to lose.

Another subtle mistake is treating PPF as a short-term parking spot. Because of the lock-in, using it for goals shorter than seven years defeats the purpose. Keep it strictly for long-term objectives.

Conclusion

The Public Provident Fund remains one of the most reliable tools in the Indian investor’s toolkit. Its EEE status provides a level of tax efficiency that is unmatched by most other instruments. By understanding how interest is credited-specifically the importance of the 5th-day rule-and leveraging the extension options, you can turn a simple savings account into a powerful retirement engine. In a world of volatile markets and changing tax laws, the certainty of PPF offers peace of mind that is worth its weight in gold.

Can I transfer my PPF account from one bank to another?

Yes, you can transfer your PPF account from one post office or bank to another. You need to fill Form PF IV and submit it to the present account holder. The transfer process usually takes 30-60 days. Ensure all dues are cleared before initiating the transfer.

What happens if I forget to deposit money for a year?

If you fail to deposit the minimum amount of ₹500 in a financial year, your account becomes inactive. To reactivate it, you must pay the minimum contribution for the inactive year(s) plus a penalty of ₹50 for each year of inactivity. The maximum number of consecutive inactive years is 15.

Is PPF interest really tax-free?

Yes, the interest earned on PPF is completely tax-free under Section 10(11) of the Income Tax Act. You do not need to include it in your total income while filing your returns. This applies to both the annual interest and the final maturity amount.

Can my spouse and I both have PPF accounts?

Yes, both spouses can have individual PPF accounts. Each person can claim a separate deduction of up to ₹1.5 lakh under Section 80C. However, you cannot open a PPF account in the name of your minor child; you can only open it for yourself or as a guardian for a minor until they turn 18.

How is the PPF interest rate decided?

The interest rate is determined by the National Housing Bank (NHB) based on market yields and government debt issuance costs. It is reviewed quarterly and announced by the Ministry of Finance. The rate is fixed for the entire financial year once declared.