Remittances with Stablecoins: Why Digital Dollars Beat Traditional Bank Transfers

Apr, 4 2026

Apr, 4 2026

Sending money across borders has always felt like a chore. You deal with predatory exchange rates, wait days for the funds to land, and wonder where your money actually is while it bounces between five different banks. But the physics of moving money is changing. Using stablecoin remittance is the process of using blockchain-based tokens pegged to a stable asset, like the US Dollar, to transfer value across borders instantly. It's not just for crypto enthusiasts anymore; it's becoming a viable alternative to the slow, expensive "legacy rails" we've used for decades.

The Quick Breakdown: Stablecoins vs. Traditional Banks

If you're looking for the bottom line, here is how the new way stacks up against the old way. Traditional systems rely on correspondent banking-essentially a chain of banks that all take a small cut and a few days to process a request. Stablecoins cut out the middleman entirely.

| Feature | Legacy Banking (SWIFT) | Stablecoin Rails |

|---|---|---|

| Average Cost | 6.49% (World Bank 2025) | Under 1% |

| Settlement Speed | 3 to 5 Business Days | Seconds to Minutes (T+0) |

| Availability | Banking Hours (Mon-Fri) | 24/7/365 |

| Transparency | Opaque / Bank Statements | Immutable Public Ledger |

Why the "Legacy Rails" Are Breaking

For years, we've relied on the SWIFT network, which is basically a messaging system that tells banks to move money. It doesn't actually move the money; it just sends the instructions. This creates a massive lag. If you're a migrant worker sending money home to support family, a 6% fee isn't just a number-it's a significant chunk of your grocery budget. According to World Bank data from 2025, these costs remain stubbornly high because of the layers of intermediary banks involved.

Stablecoins solve this by turning the money into a digital token. Instead of asking a bank in New York to tell a bank in Manila to release funds, you simply send the tokens. The settlement happens on the blockchain, meaning the moment the transaction is confirmed, the money is there. No batching, no cut-off times, and no "waiting for the bank to open on Monday."

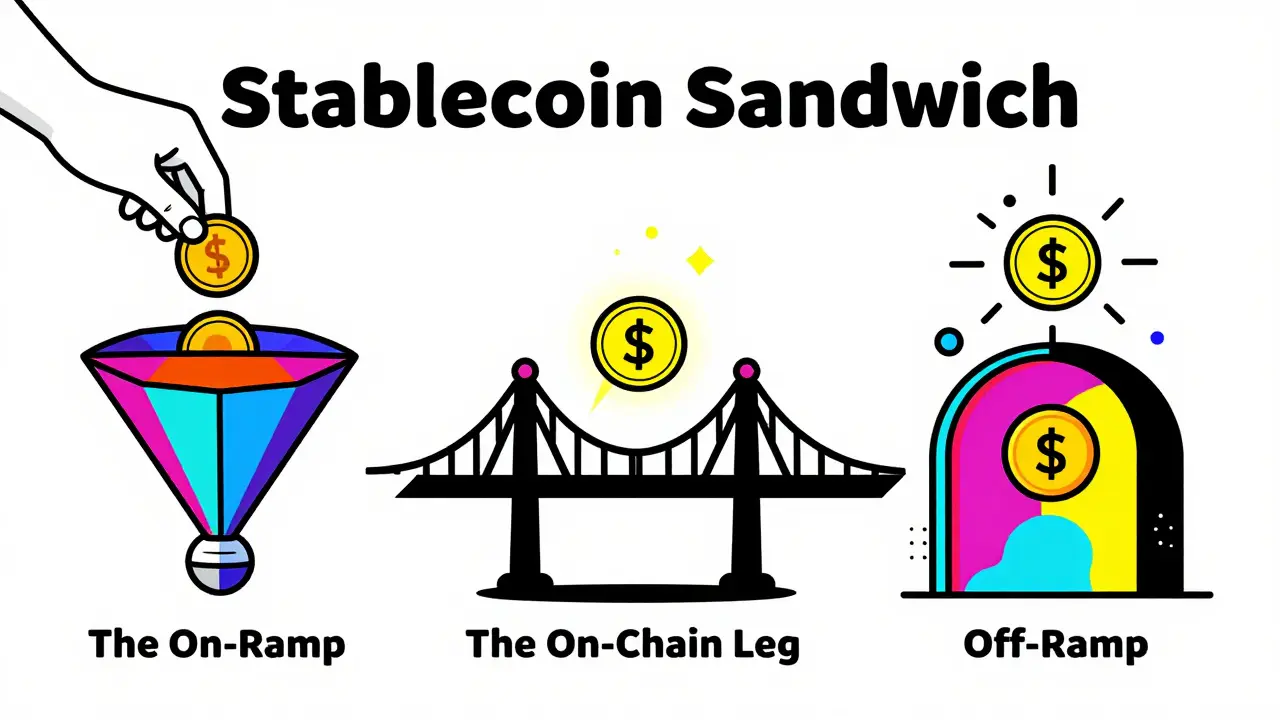

The "Stablecoin Sandwich": How It Actually Works

You don't actually need to be a blockchain expert to use this. Most modern platforms use what's called a "stablecoin sandwich." Here is the step-by-step process of how a typical transfer happens today:

- The On-Ramp: The sender deposits local fiat currency (e.g., GBP or USD) into a platform. The platform instantly converts this to a stablecoin like USDC (issued by Circle) or USDT (issued by Tether).

- The On-Chain Leg: The stablecoin is sent across a blockchain. Depending on the network, this is nearly instant. For instance, transfers on Stellar or Solana often settle in seconds with fees as low as $0.01.

- The Off-Ramp: The recipient receives the stablecoin and immediately converts it back into their local currency (e.g., Nigerian Naira or Vietnamese Dong) via a local exchange or digital wallet.

This model hides the technical complexity. The user just sees "Send Money" and "Receive Money," while the blockchain does the heavy lifting in the middle. This approach allows companies to launch new payment corridors in a matter of weeks rather than the months it takes to establish traditional banking relationships.

Solving the Compliance Nightmare

One of the biggest myths is that stablecoins are a "wild west" for money laundering. In reality, the new rails are often more compliant than the old ones. Traditional banks rely on post-facto audits-they check if something was wrong after the money has already moved. Stablecoin platforms are moving toward "embedded compliance."

Using smart contracts, platforms can bake KYC (Know Your Customer) and AML (Anti-Money Laundering) checks directly into the transaction flow. If a wallet address is flagged on a sanctions list, the smart contract can automatically block the transfer before it even happens. Regulatory frameworks like MiCA in Europe and the GENIUS Act in the U.S. are forcing issuers to hold 1:1 reserves, making these tokens as reliable as the cash they represent.

Who Benefits the Most?

While big corporations are eyeing this for B2B payments, the real impact is felt by small businesses and individuals. Imagine a freelance designer in Lagos working for a client in Berlin. In the old world, that designer might lose 5% to fees and wait a week for payment. With a stablecoin rail, they can receive a payment in USDC and have it in their local account within minutes. This improves cash flow and eliminates the stress of volatile exchange rates.

We're seeing a massive trend in regions with high inflation. In countries where the local currency loses value daily, holding a dollar-pegged stablecoin isn't just about the transfer speed-it's about preserving the value of their hard-earned money. This is why adoption is skyrocketing in India and Southeast Asia, as noted in the 2025 Global Adoption Index by Chainalysis.

The Roadblocks: What's Stopping Everyone?

If it's so much better, why isn't everyone doing it? There are still a few hurdles. First, there is the "off-ramp" problem. It's easy to get money into a stablecoin, but in some parts of Africa or Central Asia, finding a reliable way to turn those tokens back into spendable local cash can be tricky. Second, there is a technical barrier. While platforms are getting better, setting up a digital wallet still intimidates a lot of people who are used to walking into a physical bank branch.

Then there is the regulatory gray area. Some governments are still undecided on how to classify these assets. However, the trend is moving toward legitimacy. When you see the World Bank reporting that stablecoin corridors now cover 75% of major remittance flows, it's clear that the tide has turned.

Are stablecoins actually safe for sending money?

It depends on the coin. Regulated stablecoins like USDC are generally considered safe because they are backed by 1:1 reserves of cash and US Treasuries and undergo regular third-party audits. Always check if the issuer follows regulations like MiCA or the GENIUS Act before sending large sums.

How much cheaper is this than Western Union or Wise?

While Wise is already quite efficient, stablecoin rails often push fees below 1%, whereas traditional legacy systems can still average over 6% globally. The main saving comes from eliminating intermediary banks that each take a slice of the transaction.

Do I need a crypto wallet to use stablecoin remittances?

Not necessarily. Many modern fintech platforms act as the custodian. They handle the wallet and the blockchain interaction in the background, so you just interact with a standard app interface using your local currency.

How long does a stablecoin transfer actually take?

On networks like Solana or Stellar, the transfer itself happens in seconds. The only "wait time" occurs during the on-ramp and off-ramp phases (converting fiat to stablecoin and back), but even then, it's usually a matter of minutes, not days.

What happens if the stablecoin loses its peg?

This is called "de-pegging." While rare for top-tier regulated coins, it's a risk. This is why using coins with transparent, audited reserves is critical. Most remittance platforms minimize this risk by converting funds back to local fiat immediately upon arrival.

Next Steps: How to Get Started

If you're a business owner or someone sending money home, don't jump in blindly. Start by identifying a compliant provider. Look for platforms that offer transparent reserve reports and have established off-ramps in the destination country. If you're dealing with a high-volume corridor, test a small amount first to see how long the local currency conversion takes. As the infrastructure matures, the goal is a world where moving money across the globe is as simple and cheap as sending an email.