Senior Citizen Savings Scheme (SCSS) in India: Reliable Retirement Income for Seniors

Feb, 23 2026

Feb, 23 2026

When you’re past 60, your income shouldn’t vanish just because you stopped working. In India, the Senior Citizen Savings Scheme (SCSS) is a government-backed savings program designed specifically for retirees aged 60 and above to generate steady, risk-free monthly income. It’s not a stock market gamble. It’s not a risky mutual fund. It’s a simple, secure, and officially backed way to turn your savings into a reliable paycheck.

Who Can Open an SCSS Account?

You don’t need to be rich. You don’t need to be a former CEO. You just need to be 60 or older. If you’re between 55 and 59 and have retired from service-whether from government, private sector, or self-employment-you can open one too. The scheme is open to Indian citizens only. Non-resident Indians (NRIs) are not eligible. You can open the account individually or jointly with your spouse. But here’s the catch: only one of you can be the primary account holder, and the spouse must be named as a joint holder from the start. No adding a child later.

The minimum deposit is ₹1,000. You can put in up to ₹30 lakh in total across all SCSS accounts you own. That’s a lot of money, but it’s also a ceiling. If you have ₹50 lakh to invest, you can only use ₹30 lakh here. The rest needs to go elsewhere. And yes, you can open multiple accounts, but the total across all of them still can’t exceed ₹30 lakh.

How Does the Interest Work?

The interest rate isn’t fixed for life. It changes every quarter, set by the Ministry of Finance. As of January 2026, the rate is 8.2% per year. That’s higher than most bank fixed deposits. It’s paid quarterly, every three months. So if you deposit ₹20 lakh, you’ll get ₹41,000 every three months. That’s ₹164,000 a year. No taxes deducted at source. But you still have to declare it in your income tax return. It’s taxable under ‘income from other sources’.

Unlike bank FDs, where the rate locks in for the full term, SCSS rates can go up or down. But once you open the account, your rate is locked in for the entire five-year term. Even if the government raises rates next month, your account won’t benefit. If they cut rates, your rate stays the same. That’s the trade-off: stability over flexibility.

Term, Extension, and Withdrawals

The standard term is five years. That’s not a typo. It’s not 10, not 15. Five. But here’s the good part: you can extend it for another three years after maturity. You don’t have to withdraw. You can roll it over. And you can do this only once. After the extension, the account closes. No more renewals.

You can withdraw money early-but only in emergencies. If you close the account before five years, you lose 1.5% of the interest. If you close it after one year but before five, you get back your principal and the interest earned, minus that penalty. After one year, you can’t get your money back without paying this fee. That’s meant to discourage impulsive withdrawals.

Where Can You Open an SCSS Account?

You can open it at any authorized bank or post office. Most major banks like SBI, HDFC, ICICI, and PNB offer it. But many seniors find the post office easier. No online forms. No complex paperwork. Just walk in with your ID, proof of age, and a passport-sized photo. You’ll need your Aadhaar card and PAN. If you’re retiring from a job, you’ll also need a retirement certificate. Some banks ask for salary slips or pension letters. Post offices rarely do.

The process takes less than an hour. You fill a simple form. You deposit cash or a cheque. You get a passbook. That’s it. No app to download. No login to remember. Just your passbook and your ID. For people who aren’t tech-savvy, this matters.

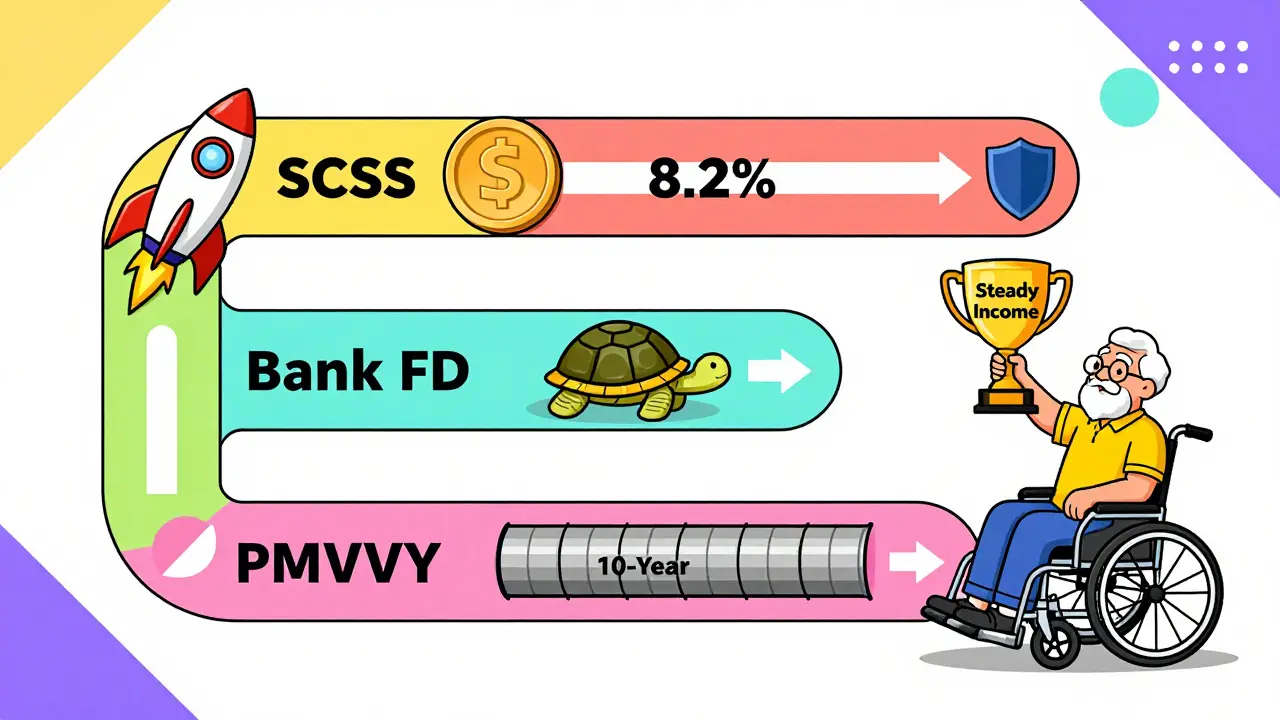

Why SCSS Beats Other Retirement Options

Let’s compare it to other common choices.

| Feature | SCSS | Bank FD | PMVVY |

|---|---|---|---|

| Interest Rate (Jan 2026) | 8.2% | 6.5% - 7.5% | 7.4% |

| Term | 5 years (extendable) | 1 to 10 years | 10 years |

| Interest Payout | Quarterly | Monthly/Quarterly/Annual | Monthly |

| Maximum Investment | ₹30 lakh | No limit | ₹15 lakh |

| Early Withdrawal Penalty | 1.5% | Varies (often 1-2%) | No early withdrawal |

| Government Guarantee | Yes | No (bank risk) | Yes |

SCSS gives you the highest rate among these three. Bank FDs are flexible but offer lower returns. PMVVY (Pradhan Mantri Vaya Vandana Yojana) has a longer term and monthly payouts, but you can’t invest more than ₹15 lakh and you can’t withdraw early. SCSS gives you more control, better returns, and the safety of a government-backed scheme.

Tax Benefits and Reporting

There’s no tax deduction under Section 80C for SCSS deposits. You can’t reduce your taxable income by putting money in. But you also don’t pay tax when you deposit. The benefit comes later: you get interest every quarter, and you pay tax on it as it comes in. If your total income is below ₹5 lakh, you pay zero tax. Many seniors fall into this bracket.

You’ll get Form 16A from the bank or post office each year showing the interest paid. Keep it. File it with your return. If you’re not filing taxes, you still need to report this income. Ignoring it can lead to notices from the tax department. It’s not a secret account. It’s a public one.

What Happens If You Pass Away?

If the primary account holder dies, the account is closed. The balance-principal plus interest-goes to the joint holder. If there’s no joint holder, it goes to the nominee. Nominees aren’t owners. They’re just receivers. If there’s no nominee, the legal heirs must claim it through a succession certificate. That’s why naming a nominee matters. It saves your family months of paperwork.

Don’t assume your will covers this. SCSS accounts operate under separate rules. The nominee overrides your will. So if you want your daughter to get it, make sure she’s named as the nominee. Not just mentioned in your will.

Common Mistakes Seniors Make

- Waiting until 65 to open it. The earlier you open it after turning 60, the sooner you start earning.

- Putting all savings into SCSS. It’s great, but not a full retirement plan. Pair it with a small mutual fund or pension.

- Not checking the interest rate before opening. Rates change quarterly. You might miss a higher rate by waiting a month.

- Ignoring the extension window. If you don’t extend after five years, the account stops earning interest.

- Forgetting to update the nominee. Life changes. Divorce, remarriage, new children. Update your nominee.

Real-Life Example: Mrs. Gupta’s Retirement

Mrs. Gupta, 62, retired from a government job in 2024. She had ₹25 lakh in savings. She didn’t want to risk it in stocks. She didn’t trust private mutual funds. She opened an SCSS account at her local post office. She deposited ₹25 lakh. At 8.2%, she now gets ₹51,250 every three months. That’s ₹205,000 a year. She uses it to cover her medical bills, groceries, and travel to visit her grandchildren. She still has ₹5 lakh in a savings account for emergencies. She sleeps better knowing her income won’t vanish.

Is SCSS Right for You?

If you’re over 60, have savings, and want predictable monthly cash flow without risk, then yes. It’s one of the safest, highest-yielding options available. If you need liquidity, or want to leave a large inheritance, you might need other tools. But for steady income? SCSS is hard to beat.

It’s not flashy. It doesn’t promise to make you rich. But it does what it says: turns your savings into a reliable retirement income. No hype. No fine print. Just a government-backed promise.

Can I open an SCSS account if I’m 58 and retired?

Yes, if you retired from service between the ages of 55 and 59. You must provide proof of retirement, like a pension letter or employer certificate. You can open the account within one year of retirement.

Is the interest rate fixed for the entire term?

Yes. Once you open the account, your interest rate is locked in for the full five-year term-even if the government raises rates later. If you extend the account for three more years, the new rate at the time of extension will apply.

Can I deposit more than ₹30 lakh in SCSS?

No. The maximum you can deposit across all SCSS accounts is ₹30 lakh. If you have more savings, you can invest the rest in bank FDs, mutual funds, or other instruments-but only ₹30 lakh qualifies for SCSS benefits.

Can I close the account before five years without penalty?

Only in cases of extreme medical emergencies, as defined by the government. Even then, you’ll still pay a 1.5% penalty on the interest earned. Early withdrawal is discouraged and not allowed for convenience or personal reasons.

Do I need to file taxes on SCSS interest?

Yes. Although no TDS is deducted, the interest is taxable under ‘income from other sources’. You must report it in your annual income tax return. If your total income is below ₹5 lakh, you may pay zero tax, but you still need to declare it.

What happens to the SCSS account if the joint holder dies?

If the joint holder dies, the primary account holder continues to hold the account. The joint holder’s death doesn’t close the account. The account remains active under the primary holder. Only when the primary holder dies does the account get closed and transferred to the nominee or legal heir.