What Are Mutual Funds? A Complete Guide for Indian Investors

Jan, 3 2026

Jan, 3 2026

Ever looked at your bank account and wondered how to make your money grow without spending hours tracking stocks? That’s where mutual funds come in. For millions of Indians, mutual funds aren’t just a buzzword-they’re the most common way to build wealth over time. Whether you’re saving for your child’s education, a home, or retirement, mutual funds offer a simple, managed way to invest. And unlike buying individual stocks, you don’t need to be a finance expert to get started.

What Exactly Is a Mutual Fund?

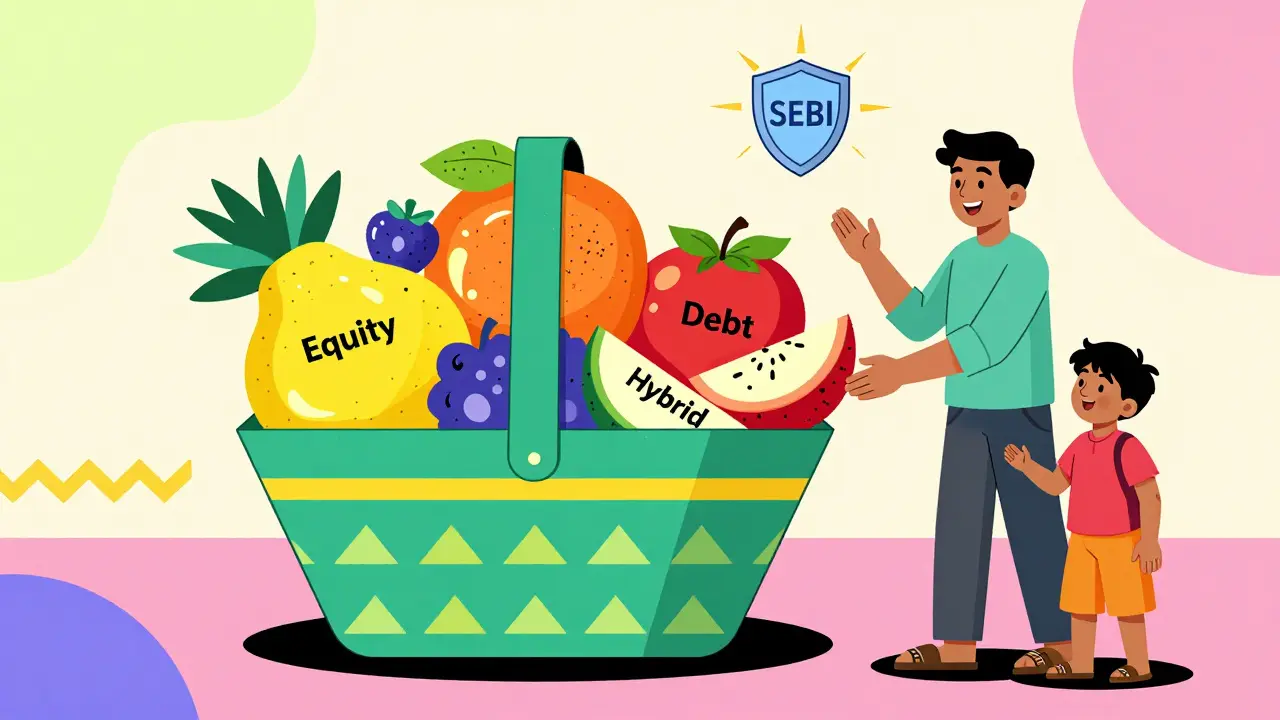

A mutual fund is a pool of money collected from many investors to buy a mix of stocks, bonds, or other securities. Think of it like a basket. Instead of picking one apple or one orange yourself, you buy a slice of a basket that already has a variety of fruits. A professional fund manager handles the buying and selling inside that basket based on the fund’s goal.

In India, mutual funds are regulated by the Securities and Exchange Board of India (SEBI). This means your money is protected by strict rules around transparency, reporting, and how fund managers can operate. Every mutual fund has a stated objective-like growth, income, or capital preservation-and the manager picks investments that match that goal.

For example, if you pick an equity mutual fund, your money goes mostly into company shares. If you choose a debt fund, it’s invested in government or corporate bonds. There are also hybrid funds that mix both. The key point: you own units of the fund, not the individual stocks or bonds inside it.

How Do Mutual Funds Make Money?

Mutual funds don’t pay you interest like a savings account. Instead, they generate returns in three ways:

- Capital appreciation-the value of the fund’s holdings goes up, so your units become worth more.

- Dividends-if the companies in the fund pay dividends, those get passed on to you.

- Interest income-if the fund holds bonds, the interest earned is distributed to investors.

Let’s say you invest ₹10,000 in a mutual fund and the fund’s value rises by 12% in a year. Your investment becomes ₹11,200. That’s your return. You don’t need to sell to see the gain-it shows up in your account statement. But if you sell, you might owe taxes depending on how long you held it.

One big advantage for Indian investors: mutual funds make it easy to invest small amounts. You can start with as little as ₹500 through a Systematic Investment Plan (SIP). That’s why over 80 million mutual fund investors in India today are regular salaried people-not millionaires.

Types of Mutual Funds in India

Not all mutual funds are the same. The type you choose depends on your goals, risk tolerance, and time horizon. Here’s a breakdown of the most common ones:

- Equity Funds-invest mostly in stocks. High risk, high potential return. Best for goals 5+ years away. Examples: large-cap, mid-cap, small-cap, sectoral funds.

- Debt Funds-invest in fixed-income securities like government bonds and corporate debentures. Lower risk, steady returns. Good for 1-3 year goals.

- Hybrid Funds-mix of equity and debt. Balanced funds and aggressive hybrid funds fall here. Reduce volatility while still growing wealth.

- Index Funds-track a market index like the Nifty 50. Low cost, passive investing. Returns mirror the index.

- ELSS Funds-Equity Linked Savings Scheme. Tax-saving mutual funds under Section 80C. Lock-in period of 3 years. Maximum deduction of ₹1.5 lakh per year.

- Money Market Funds-invest in short-term instruments like treasury bills. Very low risk, low returns. Used for parking emergency cash.

Most investors start with index funds or balanced hybrid funds because they’re simple and less stressful. If you’re saving for retirement and have 20 years to go, equity funds make sense. If you need the money in 2 years for a car, stick to debt or liquid funds.

Systematic Investment Plans (SIPs): The Indian Investor’s Secret Weapon

If you’ve heard one thing about mutual funds in India, it’s probably SIP. And for good reason. A SIP lets you invest a fixed amount-say ₹2,000-every month automatically into a mutual fund. It’s like setting up a standing order for your future self.

Here’s why SIPs work so well:

- Discipline-you invest regularly, no matter if the market is up or down.

- Cost averaging-you buy more units when prices are low, fewer when prices are high. Over time, your average cost per unit drops.

- Power of compounding-even small amounts grow big over time. Invest ₹3,000/month for 20 years at 10% annual return? You’ll have over ₹22 lakh.

Most mutual fund platforms let you start a SIP with just ₹500. You can pause, increase, or stop it anytime. No penalties. This flexibility is why SIPs are the most popular way for young professionals and middle-class families to build wealth.

How to Choose the Right Mutual Fund

With over 4,000 mutual funds in India, picking one can feel overwhelming. But you don’t need to analyze every fund. Focus on these five things:

- Goal-What are you saving for? A house in 5 years? Retirement in 20? Match the fund type to your timeline.

- Risk profile-Are you okay with your investment dropping 20% in a year? If not, avoid aggressive equity funds.

- Historical performance-Look at 5-year and 10-year returns, not just the last 12 months. Compare with the fund’s benchmark index.

- Expense ratio-This is the annual fee the fund charges. Lower is better. A fund charging 2% eats into your returns way more than one charging 0.5%.

- Fund manager track record-Has the manager been with the fund for 5+ years? Have they outperformed their peers consistently?

Don’t chase past winners. A fund that did great last year might be overvalued now. Instead, look for consistency. For example, a large-cap fund that delivered 11-13% annual returns over 10 years is better than one that jumped 25% one year and lost 15% the next.

How to Start Investing

Getting started takes less than 15 minutes. Here’s how:

- Complete your KYC-This is mandatory. You’ll need your Aadhaar, PAN, and a photo. You can do it online through any mutual fund platform or distributor.

- Choose a platform-Use apps like Zerodha Coin, Groww, Paytm Money, or direct from AMC websites like HDFC Mutual Fund or ICICI Prudential.

- Select a fund-Start with a large-cap index fund or a balanced hybrid fund. Avoid complex schemes like sectoral or thematic funds as a beginner.

- Set up a SIP-Pick your amount and date. Most platforms auto-debit from your bank account.

- Review once a year-Don’t check daily. Just make sure your fund still matches your goal and risk level.

You don’t need a financial advisor to start. Many platforms offer free tools to help you choose. Only consider an advisor if you have complex goals like estate planning or multiple income streams.

Common Mistakes Indian Investors Make

Even smart people make these errors with mutual funds:

- Chasing past performance-Buying a fund because it gave 30% last year. That’s like buying a car because it won a race last season.

- Investing too late-Waiting until you’re 40 to start. Starting at 25 with ₹2,000/month can give you ₹1.2 crore by 60. Starting at 35? You’d need to invest ₹5,000/month to reach the same.

- Ignoring taxes-Equity funds held over 1 year have long-term capital gains tax of 10% above ₹1 lakh profit. Debt funds held under 3 years are taxed at your income tax rate.

- Switching too often-Moving money every time the market dips. That’s selling low and buying high-exactly what you want to avoid.

- Not diversifying-Putting all your money in one fund or one AMC. Spread across 2-3 funds to reduce risk.

Remember: mutual funds are for the long haul. If you’re panicking during a market crash, you’re probably in the wrong fund.

What Happens When You Withdraw?

Withdrawing is easy. Log in to your platform, select the fund, and redeem your units. The money usually hits your bank account in 1-3 working days.

But timing matters:

- Equity funds-If held more than 1 year, gains above ₹1 lakh are taxed at 10%. No tax if under ₹1 lakh.

- Debt funds-If held under 3 years, gains are added to your income and taxed at your slab rate. If held over 3 years, taxed at 20% with indexation benefit.

- ELSS funds-Can’t withdraw before 3 years. After that, taxed like regular equity funds.

Always check the tax impact before redeeming. Selling for a short-term gain can wipe out your profits with taxes.

Why Mutual Funds Beat Other Options for Most Indians

Why not just keep money in a savings account? Or buy gold? Or invest in real estate?

- Savings account-Returns are around 3-4%. Inflation in India is 5-6%. You’re losing money in real terms.

- Gold-No income generation. Price swings are unpredictable. Storage and purity are issues.

- Real estate-High entry cost, low liquidity, maintenance, and legal hassles.

- Direct stocks-Requires deep knowledge, time, and emotional discipline. One bad stock can wipe out your portfolio.

Mutual funds give you diversification, professional management, low entry cost, and regulatory safety-all in one package. For 95% of Indian investors, they’re the smartest choice.

Can I lose money in mutual funds?

Yes, you can. Mutual funds are not guaranteed. Equity funds can drop 20-30% in a bad year. But over 5-10 years, markets tend to recover. The key is staying invested and not panicking. Debt funds are safer but still carry interest rate and credit risk. Never assume mutual funds are risk-free.

How much should I invest in mutual funds?

Start with what you can afford regularly-₹500 or ₹2,000 a month. A good rule: invest 10-20% of your monthly income. Don’t invest money you’ll need in the next 1-2 years. Only use surplus cash for long-term goals.

Is it better to invest directly or through a distributor?

Direct plans have lower expense ratios because you skip the advisor’s commission. You save about 0.5-1% per year. But if you’re new and need help choosing funds, a distributor can guide you. Once you understand the basics, switch to direct plans.

Do I need a Demat account to invest in mutual funds?

No. Unlike stocks, you don’t need a Demat account to invest in mutual funds. You can invest through platforms like Groww or Paytm Money without one. Only if you’re buying direct stocks or ETFs do you need a Demat account.

Can I invest in mutual funds if I’m self-employed?

Absolutely. In fact, self-employed people benefit even more because they don’t have employer-sponsored pensions. SIPs let you invest irregular amounts based on your cash flow. Just be consistent when you can.

Next Steps: What to Do Today

If you’re ready to start:

- Check your bank statement. Find out how much you can set aside monthly.

- Decide your goal: retirement, house, education?

- Go to Groww, Zerodha Coin, or a direct AMC website.

- Complete KYC (takes 10 minutes).

- Set up a ₹1,000 SIP in a large-cap index fund.

- Forget about it for 6 months.

That’s it. You’ve taken the first real step toward financial independence. Mutual funds won’t make you rich overnight. But they’ll make you richer than you’d be without them-in 10, 15, or 20 years.